Credit Score: Meaning, Importance, and How to Improve it

When I applied for my first personal loan, I was 100% confident that it would get approved. I had a decent salary, a stable job, and regular bank transactions. In my mind, everything was perfect.

Table of Contents

ToggleBut the result shocked me.

👉 My loan got rejected.

At that time, I didn’t understand the reason. After some research and discussions, I came to know about something called a credit score — and honestly, that one number completely changed my financial understanding.

If you are also planning to take a loan, use a credit card, or build your financial future, then this guide will help you deeply. I am not just explaining theory here, but also sharing what I personally experienced and learned step by step.

What is a Credit Score?

A credit score is a 3-digit number that shows how trustworthy you are when it comes to borrowing and repaying money.

In India, this score usually ranges from 300 to 900, and it is calculated by credit bureaus like CIBIL based on your financial behavior.

But instead of giving you a textbook definition, let me explain it in a practical way.

👉 Imagine you lend money to someone.

- If that person always returns money on time, you will trust them more.

- If they delay or don’t pay, you will hesitate next time.

Banks think the same way — and your credit score is the “trust score” they use.

When I checked my score for the first time, it was around 620, which falls in the risky category. That’s why my application didn’t even get proper consideration.

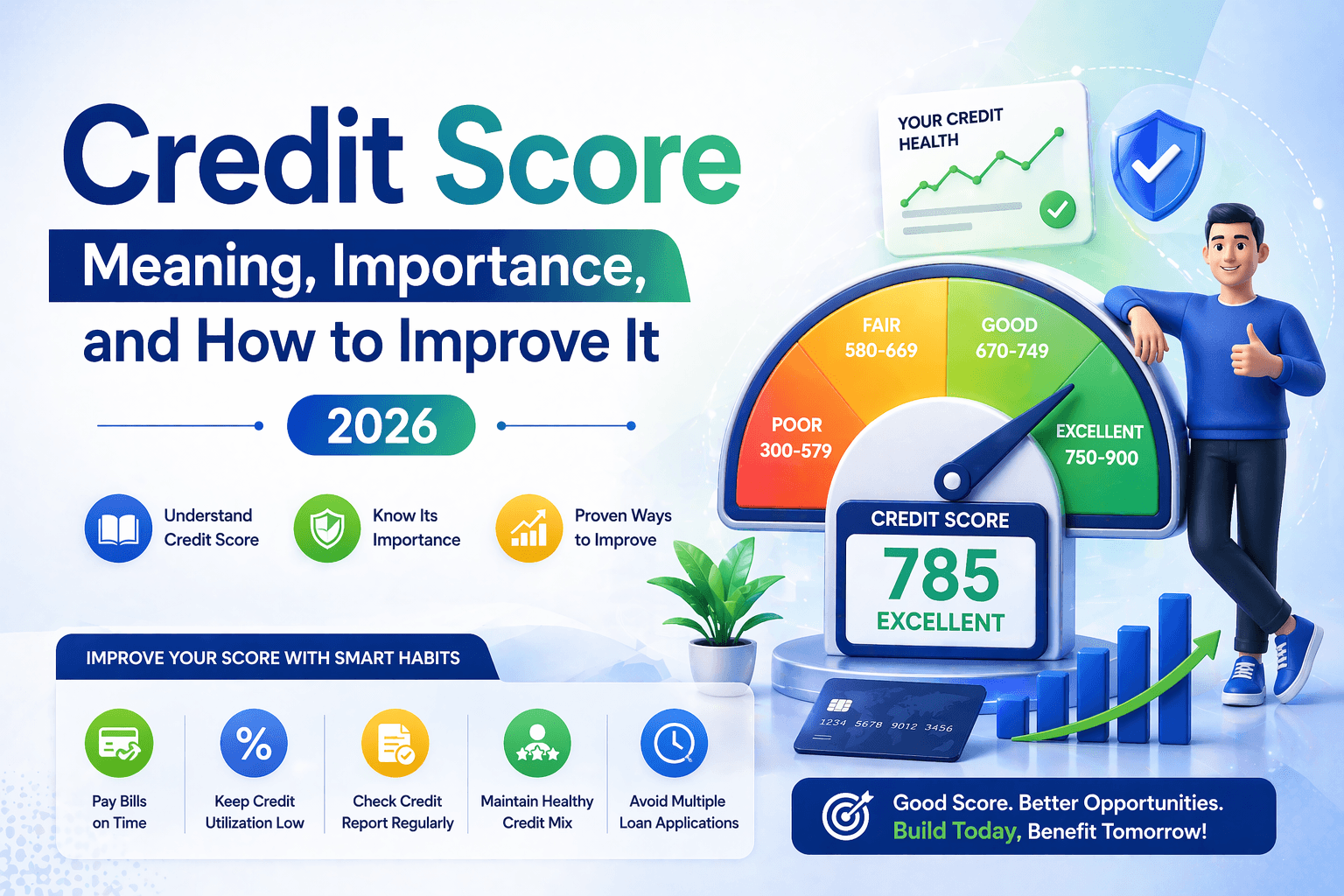

Credit Score Range: What Each Number Actually Means

Understanding the range is very important because this is exactly how lenders judge you.

- 750 – 900 (Excellent): If your score is in this range, banks treat you like a premium customer. Loan approval is fast, and you get lower interest rates.

- 650 – 749 (Average): You may get a loan, but conditions might not be very favorable.

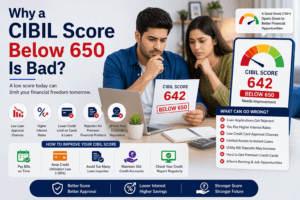

- Below 650 (Poor): This is where problems start. High chances of rejection or very high interest rates.

👉 In my case, being in the “below 650” category was the main reason behind rejection.

Why is Credit Score Important.?

Before my rejection, I used to think salary and job are everything. But after facing reality, I understood that credit score is even more important than income in many cases.

Let me explain why.

1. Loan Approval Depends on It

The first thing lenders check is your credit score — even before salary sometimes.

If your score is low, your application can be rejected instantly without deep review.

👉 This is exactly what happened to me. My salary was fine, but my score blocked me.

2. Interest Rate is Directly Linked

Even if your loan gets approved with a low score, you will pay more interest.

That means:

- Same loan amount

- Same tenure

- But higher total repayment

So indirectly, a low score makes your loan more expensive.

3. Credit Card Benefits

Once my score improved, I noticed a big change.

Earlier:

- Applications rejected

- Low limit offers

Later:

- Higher limit cards

- Better offers

- Pre-approved deals

This is when I realized how powerful a good score can be.

4. Builds Your Financial Identity

Your credit score is like your financial report card.

It tells lenders:

- Are you responsible?

- Do you pay on time?

- Can you be trusted with money?

What Actually Affects Your Credit Score (My Mistakes Included)

After my rejection, I didn’t just accept it — I analyzed everything deeply. And I found some mistakes which most people unknowingly make.

1. Payment History (Biggest Factor)

This is the most important part.

Even a small delay in EMI or credit card payment can hurt your score.

👉 I once delayed a credit card payment by just a few days, and it stayed in my report.

Lesson: Always pay on time — no excuses.

2. Credit Utilization Ratio

This means how much credit you are using compared to your limit.

Earlier, I used almost my full limit because I thought it’s okay.

But actually:

- High usage = risky behavior

- Low usage = controlled behavior

👉 After I reduced my usage below 30%, my score started improving.

3. Too Many Loan Applications

This was my biggest mistake.

I applied on multiple apps thinking “kahi na kahi se mil hi jayega”.

But every application created a hard inquiry, which reduced my score further.

4. No Proper Credit Mix

Only using one type of credit is not ideal.

Having a mix like:

- Credit card

- Small loan

can improve your profile.

5. Short Credit History

If you are new to credit, your score may be low simply because there is not enough data.

My Step-by-Step Journey to Improve My Credit Score

Instead of giving random tips, let me tell you exactly what worked for me.

Step 1: I Checked My Full Credit Report

Not just the score — I checked details.

I found:

- Late payment record

- High credit usage

This clarity helped me plan.

Step 2: I Became Strict with Payments

I set reminders and made sure:

- No EMI delay

- No credit card delay

This alone started improving my score within weeks.

Step 3: I Controlled My Spending

Earlier, I used my credit card like extra income.

Now:

- Limited usage

- Planned expenses

👉 This changed everything.

Step 4: I Stopped Random Applications

Instead of applying everywhere, I waited and applied smartly.

Step 5: I Built Positive History

I took a small loan and repaid it properly.

This added positive data to my report.

Read More:Why a CIBIL Score Below 650 Is Bad?

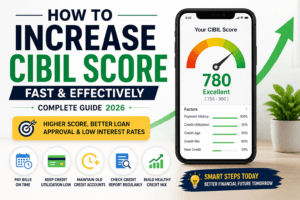

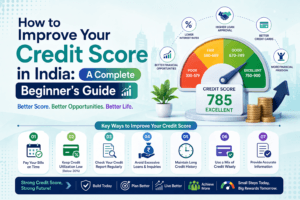

Proven Tips to Improve Your Credit Score

If you follow these steps consistently, results will definitely come.

- Pay Everything On Time

This is non-negotiable. Even one missed payment can damage your score. - Keep Credit Usage Low

Ideal: Below 30% - Avoid Multiple Applications

Apply only when necessary. - Monitor Your Credit Report

Check for errors and fix them. - Keep Old Accounts Active

Old accounts help build history.

How Long Does It Take to Improve Credit Score?

Based on my real experience:

- Small improvement → 1–2 months

- Good improvement → 3–6 months

There is no shortcut — consistency is the key.

Common Mistakes You Should Avoid

These are very common but dangerous:

- Applying on many apps

- Ignoring small dues

- Using full credit limit

- Closing old accounts

- Not checking credit report

Avoiding these alone can save your score.

Conclusion

If you ask me one thing that changed my financial life, it would be understanding my credit score.

Earlier, I faced rejection and frustration.

Now:

- Better approvals

- Better offers

- More confidence

👉 The best part is — anyone can improve their score with discipline.

It doesn’t matter if your score is low today.

What matters is what you do next.