Losses of Credit Repair When Trying to Get a Loan

In today’s fast-moving financial world, getting a loan has become easier—but only for those who understand how the system truly works. Many people believe that using credit repair services is the fastest way to improve their credit score and secure loan approval. On the surface, this sounds like a smart move. However, the reality is very different.

Table of Contents

ToggleThe losses of credit repair when trying to get a loan are often ignored or misunderstood. Instead of helping, credit repair can sometimes delay your loan approval, reduce your credibility in the eyes of lenders, and even lead to rejection. This happens because lenders don’t just look at your credit score—they analyze your complete financial behavior, history consistency, and risk profile.

In this detailed guide, we will uncover the hidden risks, disadvantages, and real impact of credit repair services on your loan approval. Whether you are planning to apply for a personal loan, business loan, or credit card, this article will help you avoid costly mistakes and make smarter financial decisions.

What is Credit Repair.?

Credit repair is the process of improving your credit score by correcting errors, removing negative marks, or managing outstanding debts. This can be done either by yourself or through third-party credit repair companies.

These services usually promise:

- Removal of negative entries

- Improvement in credit score

- Faster loan approval

But here’s the catch: not all improvements are genuine or sustainable, and lenders can detect manipulated or unstable credit profiles.

Major Losses of Credit Repair When Trying to Get a Loan

1. Temporary Credit Score Boost (Not Trusted by Lenders)

One of the biggest problems with credit repair is that the improvement is often temporary. Some companies use short-term techniques like disputing entries or restructuring data to boost your score.

However, lenders look beyond just numbers. They analyze:

- Consistency of your credit history

- Repayment behavior over time

- Stability of financial activity

If your score suddenly increases without strong financial backing, lenders may consider it suspicious.

👉 Result: Your loan application may get delayed or rejected.

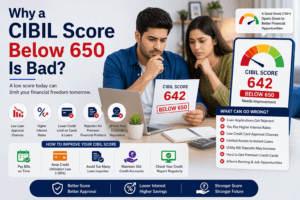

Read More: Why a CIBIL Score Below 650 Is Bad?

2. Negative Impact on Credit History Transparency

When credit repair companies remove certain entries (even legally), it can create gaps in your credit history.

Lenders prefer:

- Long and stable credit history

- Transparent financial behavior

If your report looks “clean but incomplete,” it raises red flags.

👉 Loss: Reduced trust from lenders, lower approval chances.

3. High Risk of Credit Repair Scams

Many credit repair services promise unrealistic results like:

- “100% loan approval guaranteed”

- “Instant CIBIL score increase”

In reality, such claims are misleading.

Common scam practices:

- Charging high upfront fees

- Filing fake disputes

- Providing false documentation

👉 Loss: Financial loss + possible legal issues + damaged credit profile.

4. Delay in Loan Approval Process

Credit repair is not an instant process. It can take:

- 30 to 90 days (or more)

- Multiple dispute cycles

If you urgently need a loan, relying on credit repair can delay your application.

👉 Loss: Missed opportunities (business, emergency, investment).

5. Disputes Can Backfire

When you raise disputes on your credit report:

- The lender verifies the information

- If found correct, it stays permanently

Frequent or unnecessary disputes can:

- Make your profile look unstable

- Reduce your credibility

👉 Loss: Lower trust score from lenders.

6. No Guarantee of Loan Approval

Even after credit repair, loan approval depends on multiple factors:

- Income stability

- Employment type

- Existing liabilities

- Debt-to-income ratio

A better score does not guarantee approval.

👉 Reality: Credit repair is not a shortcut to loan approval.

7. Increased Financial Burden

Credit repair services are not free. You may pay:

- Monthly service fees

- Consultation charges

- Processing fees

If the results are not effective, it becomes an unnecessary expense.

👉 Loss: Money wasted without real financial improvement.

8. Artificial Credit Behavior Detection

Modern lenders and NBFCs use advanced algorithms to detect:

- Sudden score jumps

- Unusual account changes

- Frequent disputes

This is especially common in India with stricter lending policies.

👉 Loss: Profile marked as risky.

How Credit Repair Affects Loan Approval in Reality

Let’s understand how lenders actually evaluate your application:

Key Factors Lenders Check

- Credit score (CIBIL score)

- Repayment history

- Income and job stability

- Existing loans and EMIs

- Financial discipline

Even if your score improves through credit repair, lack of real financial improvement will still lead to rejection.

Common Credit Repair Mistakes to Avoid

- Relying Completely on Third-Party Services

Always verify what changes are being made to your report.

2. Ignoring Real Debt Repayment

Clearing dues is more important than hiding them.

3. Applying for Loan Immediately After Repair

Give your profile time to stabilize.

4. Falling for “Guaranteed Approval” Claims

No one can guarantee loan approval.

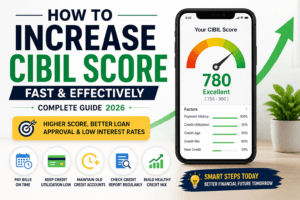

Better Alternatives to Credit Repair (Smart Strategy)

Instead of risky credit repair, follow these proven methods:

- Pay EMIs on Time

This builds genuine credit trust.

- Reduce Credit Card Utilization

Keep usage below 30%.

- Avoid Multiple Loan Applications

Too many inquiries reduce your score.

- Maintain Long-Term Credit Stability

Consistency matters more than quick fixes.

Read More: Best Instant Personal Loan Apps in India

Real Example: Why Credit Repair Fails

Imagine two borrowers:

Person A (Credit Repair User):

- Score improved from 600 to 750 in 1 month

- Used disputes and removals

- No income growth

Person B (Organic Improvement):

- Score improved from 600 to 720 in 6 months

- Paid dues regularly

- Stable income

👉 Lenders will prefer Person B, because their profile shows real financial discipline.

FAQs (Frequently Asked Questions)

Q1. Does credit repair really help in loan approval?

Credit repair may improve your score temporarily, but loan approval depends on multiple factors like income, repayment history, and financial stability.

Q2. Can credit repair hurt my chances of getting a loan?

Yes, if done improperly, it can create inconsistencies in your credit report and reduce lender trust.

Q3. Is credit repair legal in India?

Yes, correcting genuine errors is legal. However, fake disputes or misleading practices can create problems.

Q4. How long should I wait after credit repair before applying for a loan?

It is advisable to wait at least 2–3 months to ensure your credit profile stabilizes.

Q5. What is better: credit repair or improving credit naturally?

Natural improvement is always better as it builds long-term trust with lenders.

Q6. Do all lenders check detailed credit history?

Yes, most banks and NBFCs analyze complete credit behavior, not just the score.

Conclusion

The idea of credit repair may seem attractive, especially when you need urgent loan approval. However, as we’ve explored in detail, the losses of credit repair when trying to get a loan can outweigh the benefits if not handled carefully.

Credit repair is not inherently bad—but relying on it blindly, especially through third-party agencies, can damage your financial credibility. Lenders today are smarter, more data-driven, and highly focused on long-term financial behavior rather than short-term score improvements.

If your goal is to get approved for a loan, focus on building genuine financial strength instead of chasing shortcuts. Pay your dues on time, maintain a stable income, and improve your credit profile organically. This approach not only increases your approval chances but also ensures better loan terms, lower interest rates, and long-term financial stability.

Remember:

👉 A strong financial profile is built over time—not repaired overnight.