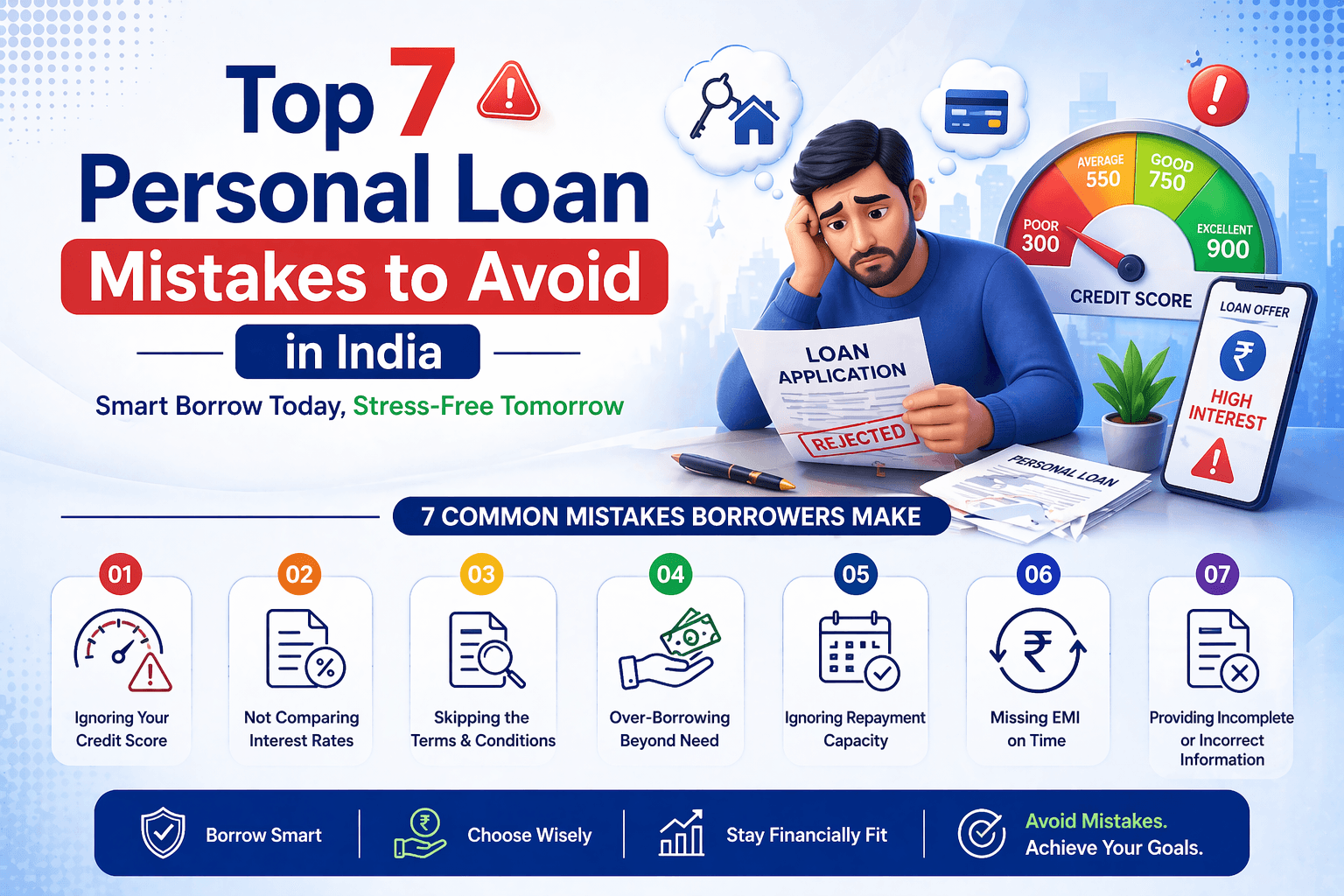

Top 7 Personal Loan Mistakes

In today’s time, taking a personal loan has become extremely easy—just a few clicks and the money gets credited to your account. But this very convenience often pushes people toward making serious mistakes, the cost of which is later paid through heavy EMIs, financial stress, and a poor credit score.

From my own experience working in the finance industry and observing real customer cases, I’ve realized that most people tend to ignore small but crucial details before taking a loan. These minor oversights eventually turn into major financial problems.

In this blog, we will understand in detail what a personal loan mistake really is, and explore the top 7 major mistakes that you must avoid at all costs.

Table of Contents

Toggle1. Taking a Personal Loan Without Need

Many people take a loan just because they see “eligibility” or keep receiving offers from banks and apps.

But the truth is, every loan is a liability, not income.

What goes wrong?

- People take loans for luxury items (mobile, trips, shopping)

- They don’t differentiate between needs and wants

- They ignore future EMI burden

Real Insight:

One of my clients took a ₹1.5 lakh loan just for a vacation. The EMI was manageable, but after 6 months, he lost his job—and the same loan became a burden.

What should you do?

- Ask yourself: “Is this really necessary?”

- Avoid loans if savings can cover the expense

- Take loans only for emergencies or productive purposes

2. Not Comparing Interest Rates (Avoid personal Loan Mistakes)

This is one of the most common personal loan mistakes. People often take a loan from the first bank or app they come across.

What’s the problem?

- Interest rates can vary from 10% to 24%

- Processing fees and hidden charges increase the cost

- Total repayment becomes much higher

Example:

₹2 lakh loan

- Bank A: 11% interest

- App B: 20% interest

Difference: ₹25,000+ extra repayment

What should you do?

- Compare at least 3–4 lenders

- Check banks, NBFCs, and fintech apps

- Focus on total loan cost, not just EMI

Read More:

Why a CIBILScore below 650 is bad.?3. Ignoring Your Credit Score

Not checking your credit score before applying is a big mistake.

Impact:

- Low score = Higher interest rate

- Loan rejection chances increase

- Financial credibility gets affected

Ideal Score:

- 750+ = Best rates

- 650–750 = Average

- Below 650 = Risk zone

Real Case:

An applicant had a good salary but a credit score of 620. He still got a loan—but at 22% interest.

What should you do?

- Check your credit report before applying

- Pay EMIs on time

- Clear credit card dues regularly

4. Miscalculating EMI Capacity

Many people don’t plan their EMI affordability properly.

Common mistakes:

- Deciding EMI based only on current salary

- Ignoring future expenses

- Not maintaining an emergency fund

Thumb Rule:

Your EMI should not exceed 30–40% of your monthly income.

Real Insight:

A person earning ₹40,000 took an EMI of ₹18,000. Within months, expenses increased and he started defaulting.

What should you do?

- Use EMI calculators

- Include future expenses in planning

- Keep an emergency fund (3–6 months)

5. Not Reading Loan Terms & Conditions

This is a silent but dangerous mistake.

Hidden traps:

- Prepayment charges

- Foreclosure fees

- Late payment penalties

- Insurance costs

What happens?

The loan seems cheap initially, but becomes expensive due to hidden charges.

Example:

₹3 lakh loan

- Processing fee: ₹6,000

- Insurance: ₹4,000

Total hidden cost = ₹10,000

What should you do?

- Read the agreement carefully

- Never ignore the fine print

- Ask the lender if anything is unclear

Read More:

Fast Approved Personal Loan in 20266. Taking Multiple Loans at Once

Some people take another loan even when one is already running.

Problems:

- Increased EMI burden

- High credit utilization

- Higher risk of default

Real Case:

A customer already had 2 loans. After taking a third one, total EMI became ₹25,000 while salary was ₹45,000—result: default.

What should you do?

- Close one loan before taking another

- Maintain a healthy debt-to-income ratio

- Avoid unnecessary borrowing

7. Missing or Delaying EMI Payments

This is the most dangerous personal loan mistake.

Impact:

- Credit score drops significantly

- Penalty charges apply

- Can even lead to legal action

Real Insight:

Missing just 2 EMIs can reduce your credit score by 80–100 points.

What should you do?

- Enable auto-debit

- Set payment reminders

- Inform the bank in case of delay

Key Factors That Affect personal Loan Eligibility

Credit Score (CIBIL Score)

Your credit score plays a major role in loan approval. Most lenders prefer a CIBIL score of 700 or above

2. Monthly Income

A stable income assures lenders that you can repay the loan on time. Salaried and Self-employed applicants have different income requirements.

3. Employment Type

Banks usually prefer applicants who are salaried with reputed companies of self-employed with stable business income.

4. Age of the Applicant

Most lenders allow personal loans to applicants aged between 21 to 60 years.

5. Existing Loans and EMIs

If you already have multiple loans, your eligibility may reduce. High EMI oligations increase financial risk.

6. Proper Documentation

Banks and NBFC’s are check all documents before file Login if they find any mismatch and other incomplition in documents they are rejects loan file.

7. Cash salary

For Personal loan Applicant must credited income/salary in bank account.

Read More:

How to Improve Credit Score in IndiaCommon Personal Loan Mistakes for Loan Rejection

- Low or No credit history

- High credit card usage

- Frequent loan applications

- Unstable income source

- Past Loan Defaults

How to Improve Personal Loan Eligibility

- Pay EMIs and credit card bills on time

- Maintain credit utilization below 30%

- Avoid multiple loan inquiries

- Reducce existing debt

- Check credit report for errors

Documents Required for Personal Loan

- Identity proof (Aadhar, PAN)

- Address proof

- Income proof (salary slips/ITR)

- Bank Statements

Bonus Tips: How to Be a Smart Borrower

If you want to handle loans smartly, follow these tips:

- Borrow only what you need

- Choose tenure wisely (shorter = less interest)

- Always keep a backup fund

- Define your financial goal before taking a loan

- Borrow only from trusted lenders

Final Thoughts

A personal loan is a powerful financial tool—if used wisely. But even a small personal loan mistake can disturb your entire financial life.

In my experience, people don’t fall into loan traps because they lack knowledge—they fall because they make rushed decisions.

If you avoid these 7 mistakes, you can not only save money on interest but also stay stress-free financially.

Remember: Taking a loan is easy, but managing it smartly is the real skill.

FAQs (Frequently Asked Questions)

Q1. What should I check before taking a personal loan?

You should check the interest rate, processing fee, EMI amount, credit score, and lender credibility.

Q2. Can I get a loan with a low credit score?

Yes, but the interest rate will be higher and conditions stricter.

Q3. What is a safe EMI limit?

EMI up to 30–40% of your income is considered safe.

Q4. Is prepayment of a loan a good option?

Yes, if the charges are low, it helps save interest.

Q5. Is it okay to take multiple loans?

No, it increases financial burden and risk of default.