How to Improve Credit Score in India

In today’s lending ecosystem, your credit score quietly decides almost everything—whether your loan gets approved, how fast it gets approved, and at what interest rate. I’ve seen applicants with solid salaries get rejected, while others with average income get instant approvals—simply because they managed their credit better.

Table of Contents

ToggleIf you’ve been searching for how to improve credit score, this guide goes beyond surface-level tips. It breaks down what actually works in India, why it works, and how you can apply it step by step—based on real patterns I’ve observed while dealing with loan cases.

What Is a Credit Score (And Why It Matters More Than You Think)

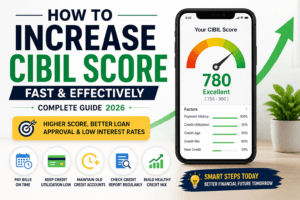

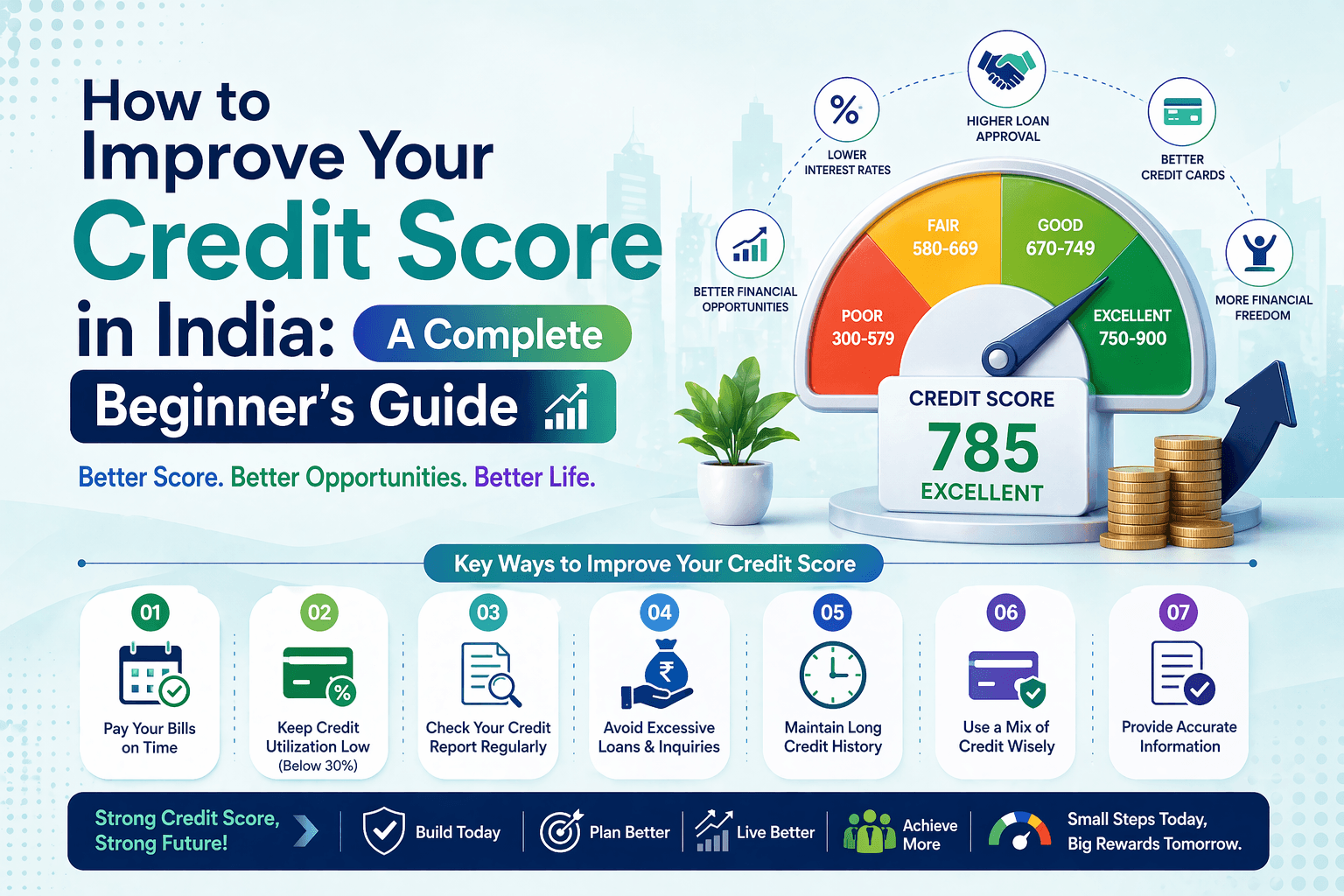

A credit score is a 3-digit number (300–900) that reflects your reliability as a borrower. Lenders don’t know you personally—they rely on this number to judge your financial discipline.

Score Ranges (India)

- 750–900: Excellent (lowest interest, fastest approvals)

- 650–749: Good (approvals possible, but not best rates)

- 550–649: Weak (high interest, stricter checks)

Below 550: High risk (frequent rejections)

Real-World Impact

- High score: Better loan deals, higher limits, faster processing

- Low score: Rejections, high interest, extra documentation

Key takeaway: Improving your score isn’t optional—it directly saves (or costs) you money.

How Your Credit Score Is Calculated (India Context)

Understanding this is crucial for anyone serious about how to improve credit score:

- Payment History (35–40%) – On-time vs late payments

- Credit Utilization (~30%) – How much of your limit you use

- Credit History Length (~15%) – Age of your accounts

- Credit Mix (~10%) – Types of credit (cards + loans)

- Hard Inquiries (~10%) – New applications

If you fix the first two—payment history and utilization—you’re already solving 65–70% of the problem.

How to Improve Credit Score (Deep, Practical Strategy)

1. Master Your Payment Discipline (Non-Negotiable)

This is the single biggest driver of your score.

What actually hurts:

- Paying after the due date (even by a few days)

- Paying only the minimum due on credit cards

- EMI bounces due to low bank balance

What actually works:

- Set auto-debit + SMS reminders (backup system)

- Pay 3–5 days before due date (not on the last day)

- Always aim for full payment, not minimum due

Real Pattern I’ve Seen: Two missed EMIs can drop a good score (780) to near 700. Recovery then takes months—not days.

2. Control Credit Utilization (The Silent Score Killer)

Utilization = (Credit used ÷ Total limit) × 100

Ideal Target:

- Below 30% overall

- For best results, keep 10–20%

Why it matters:

High usage signals dependency. Even if you pay on time, consistently high usage tells lenders you’re stretched.

Practical Tactics:

- Pay part of your bill before statement generation

Request a limit increase (without increasing spending) - Split expenses across multiple cards (if you have them)

3. Audit Your Credit Report (Fix What You Didn’t Break)

Many people lose points due to reporting errors, not behavior.

Common issues:

- Closed loans shown as active

- Late payments wrongly marked

- Duplicate accounts or unknown loans

What to do:

- Check your report from bureaus (e.g., CIBIL) periodically

- Raise a dispute for any mismatch

- Track until it’s resolved (don’t assume it will auto-fix)

Why this is powerful:

Correcting errors can instantly improve your score without changing your habits.

4. Be Strategic With Applications (Avoid “Credit Hunger” Signals)

Every loan/card application creates a hard inquiry.

What hurts:

- Applying to multiple apps/banks within days

- “Just checking eligibility” across platforms

What works:

- Use pre-approved offers first

- Space out applications (at least a few weeks)

- Apply only where your profile fits (income, job type, score)

Reality Check:

Too many inquiries in a short time window can knock off 20–40 points.

5. Preserve Your Old Accounts (Age Builds Trust)

Common mistake:

Closing your oldest credit card because you “don’t use it.”

Why that backfires:

- Reduces your average account age

- Lowers your total available limit (raising utilization %)

Smarter approach:

- Keep old cards active with small spends

- Use them once every 1–2 months and pay in full

6. Build a Healthy Credit Mix (Show You Can Handle Variety)

Lenders prefer borrowers who can manage different credit types.

Balanced profile:

- Unsecured: Credit cards, personal loans

- Secured: Auto loan, home loan, FD-backed card

If you’re new:

- Start with a secured credit card (FD-based)

- Add variety gradually—don’t rush

7. Starting From Zero or Rebuilding From Low Score

If your score is low (below 650) or non-existent, start small and controlled.

Step-by-step:

- Take a secured card against FD

- Use 10–20% of the limit monthly

- Pay 100% on time for 3–6 months

- Avoid new applications during this phase

What to expect:

- First visible jump: 2–3 months

- Strong base: 6–9 months

Advanced Moves (When You Want Faster Improvement)

- Pay twice in a billing cycle (before and after statement)

- Convert high card dues into lower-interest EMI plans (if needed)

- Avoid becoming a guarantor/co-applicant unless necessary

- Keep bank balance sufficient to avoid EMI bounces

Mistakes That Quietly Damage Your Score

- Paying only minimum due for months

- Running cards at 80–90% utilization

- Applying everywhere after one rejection

- Ignoring small dues (₹500–₹1000 can still hurt)

- Settling loans instead of closing properly

Realistic Timeline (Set the Right Expectations)

- 30–60 days: Small corrections (utilization, payments)

- 3–6 months: Noticeable improvement

- 6–12 months: Strong, stable profile

There’s no instant hack. Consistency compounds.

A Simple Monthly Routine (That Actually Works)

- Week 1: Check balances, keep utilization low

- Week 2: Make partial payment before statement

- Week 3: Review credit report (quick scan)

- Week 4: Pay full dues before due date

Repeat this for 3–6 months—you’ll see the difference.

Conclusion

How to improve credit score isn’t about tricks—it’s about habits. The people who win here are not the ones earning the most, but the ones managing credit with discipline.

If you focus on:

- On-time, full payments

- Low utilization

- Fewer, smarter applications

…your score will move in the right direction. And once it does, everything else—approvals, limits, interest rates—gets easier.

Remember: Your credit score is your financial reputation. Build it deliberately.

FAQs (Frequently Asked Questions)

Q1. How to improve credit score fast in India?

Focus on on-time full payments, keep utilization below 30%, and avoid new applications for a few months.

Q2. How long does it take to improve a credit score?

You may see changes in 3–6 months; strong improvement typically takes 6–12 months.

Q3. What is an ideal credit score?

750+ is considered excellent for best rates and quick approvals.

Q4. Can I get a loan with a low credit score?

Yes, but at higher interest and stricter terms. Improving first is usually smarter.

Q5. Does using a credit card help?

Yes—if used responsibly with low utilization and full, on-time payments.

Q6. What is credit utilization?

The percentage of your limit you use. Keep it under 30% (ideally 10–20%).

Q7. Do multiple applications hurt my score?

Yes, each creates a hard inquiry. Too many in a short time can lower your score.

Q8. How much does one missed EMI affect the score?

It can drop 50–100 points and stays on your report for years.

Q9. How do I build a score with no history?

Start with an FD-backed secured card, use lightly, and pay in full every month.

Q10. What if my credit report has errors?

Raise a dispute with the bureau and follow up until corrected—this can quickly improve your score.