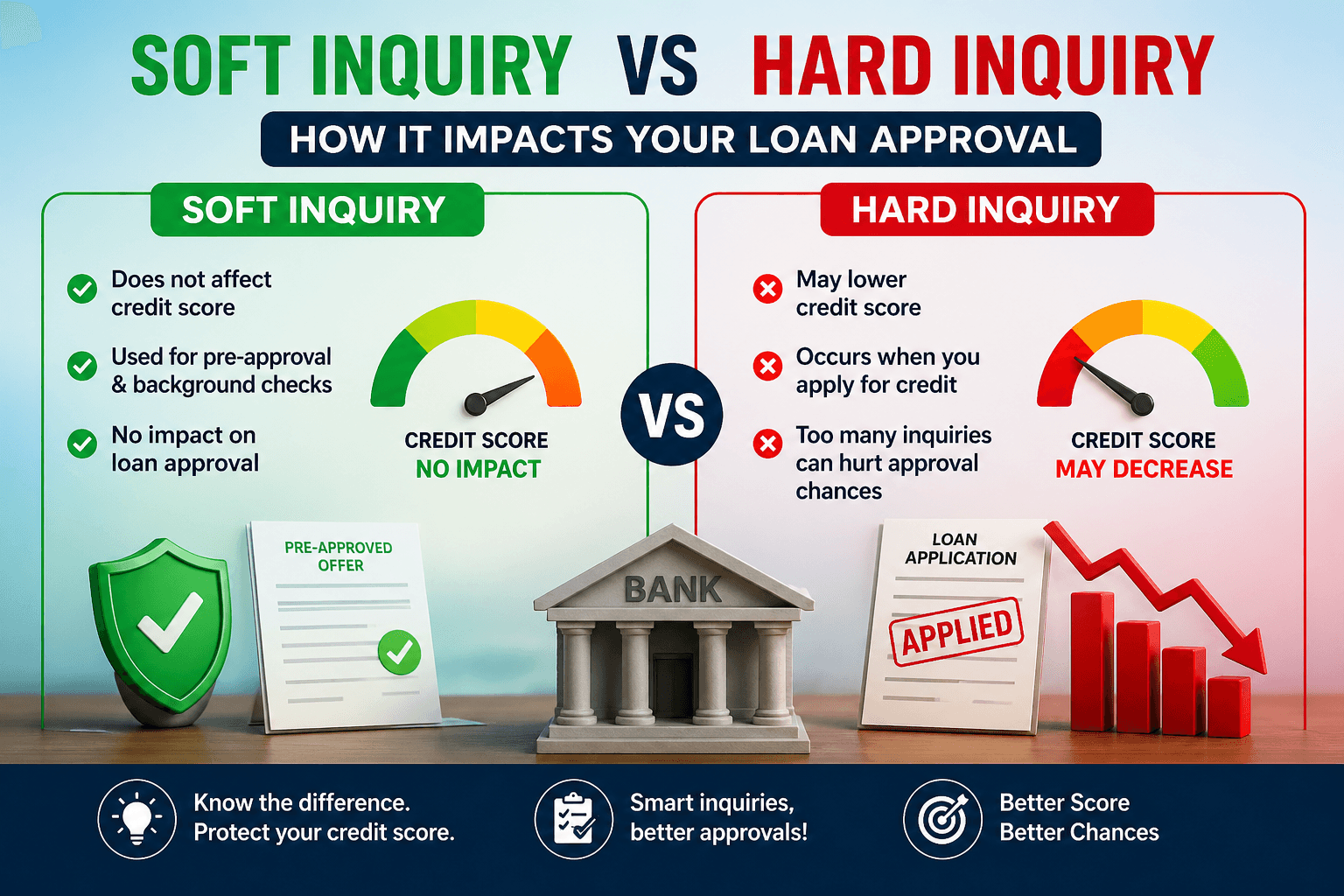

Soft Inquiry vs Hard Inquiry: How It Impacts Your Loan Approval

When you apply for a loan or check your credit score, lenders perform something called a credit inquiry. But did you know that not all inquiries are the same? Understanding the difference between a soft inquiry vs hard inquiry can directly impact your credit score, CIBIL report, and ultimately your loan approval chances.

Table of Contents

ToggleMany people unknowingly reduce their approval chances simply because they don’t understand how credit inquiries work. In this detailed guide, we will break down everything you need to know about soft vs hard credit inquiry, how they affect your credit score, and how to avoid mistakes.

What is a Credit Inquiry?

A credit inquiry happens when a lender or financial institution checks your credit report. This is done to evaluate your creditworthiness before approving loans, credit cards, or other financial products.

There are two types of credit inquiries:

- Soft Inquiry

- Hard Inquiry

Understanding the difference between soft and hard inquiry in CIBIL is essential if you want to improve your chances of loan approval.

What is a Soft Inquiry?

A soft inquiry (also called a soft pull) occurs when your credit report is checked without affecting your credit score.

Common Examples of Soft Inquiry:

- Checking your own credit score

- Pre-approved loan offers

- Background checks by employers

- Loan eligibility checks

Key Features:

- Does not affect credit score

- Not visible to lenders in most cases

- Safe to perform multiple times

So, if you’re wondering, “does checking loan eligibility affect CIBIL score?” — the answer is No, as long as it’s a soft inquiry.

What is a Hard Inquiry?

A hard inquiry (also known as a ) happens when a lender checks your credit report after you apply for credit.

Common Examples of Hard Inquiry:

- Applying for a personal loan

- Credit card application

- Home loan or car loan application

Key Features:

- Affects your credit score

- Visible to other lenders

- Multiple hard inquiries can reduce approval chances

If you’re asking, “does hard inquiry affect credit score?” — the answer is Yes.

Read More: Dark truth of Instant Loan Apps

Soft Inquiry vs Hard Inquiry: Key Differences

| Feature | soft inquiry | Hard inquiry |

|---|---|---|

|

Impact on Credit Score |

No Impact |

Slight negative impact |

|

Visibility |

Not visible to lenders |

Visible to lenders |

|

When It Happens |

Eligibility checks, self-check |

Loan/credit application |

|

Risk Level |

Safe |

Risky if repeated |

|

Approval Impact |

No effect |

Can reduce chances |

How Hard Inquiry Affects Your Credit Score

A single hard inquiry may reduce your credit score by a few points (usually 5–10 points). However, the real problem arises when there are multiple inquiries in a short time.

Why Multiple Hard Inquiries Are Risky:

- Indicates credit-hungry behavior

- Signals financial instability

- Reduces lender trust

This is why people often ask:

👉 “How many hard inquiries are too many?”

Answer:

- 1–2 inquiries: Safe

- 3–5 inquiries: Risky

- 5+ inquiries: High risk for rejection

Impact of Credit Inquiry on Loan Approval

Your loan approval doesn’t depend only on your credit score — your credit behavior also matters.

How Hard Inquiries Affect Loan Approval:

- Multiple inquiries = higher rejection chances

- Lenders assume you are desperate for credit

- Your risk profile increases

So, the credit inquiry impact on loan approval is very real and often ignored.

Soft Inquiry vs Hard Inquiry in Real Life

Let’s understand with a simple example:

Scenario 1 (Smart User):

Rahul checks loan eligibility on 3 apps → Soft inquiries → No impact → Gets loan approved

Scenario 2 (Common Mistake):

Amit applies for loans on 6 apps → Hard inquiries → Score drops → Loan rejected

This clearly shows how soft pull vs hard pull credit can affect your outcome.

Does a Hard Inquiry Hurt Your Credit Score in India?

Yes, hard inquiries do affect your CIBIL score in India.

However:

- Impact is temporary

- Stays on report for 2 years

- Major impact only in first 3–6 months

So if you’re searching:

👉 “does a hard inquiry hurt your credit score in India?”

The answer is Yes, but manageable.

Read More: Urgent ₹10000 Loan – Real Experience

Can Multiple Inquiries Reduce Loan Approval Chances?

Yes, absolutely.

Here’s how:

- Lenders see multiple applications

- Assume financial stress

- Reject application even with a decent score

So, if you’re wondering:

👉 “can multiple inquiries reduce loan approval chances?”

The answer is a strong Yes.

How Lenders Check Credit Score for Loans

Lenders follow a standard process:

1. Receive your application

2. Perform a hard inquiry

3. Analyze:

- CIBIL score

- Payment history

- Credit utilization

- Recent inquiries

This is why understanding how lenders check credit score for loans is important.

How to Avoid Hard Inquiries on Credit Report

Here are smart ways to protect your credit profile:

1. Check Eligibility First

Use platforms that perform soft inquiries before applying.

2. Avoid Multiple Applications

Apply to only 1–2 lenders at a time.

3. Compare Before Applying

Research interest rates and approval criteria.

4. Improve Your Profile First

If your score is low, fix it before applying.

5. Wait Between Applications

Keep a gap of at least 3–6 months.

Following these tips will help you avoid hard inquiries on credit report.

Soft Inquiry vs Hard Inquiry: Which is Better?

Clearly, soft inquiries are better because:

- No impact on credit score

- No risk to loan approval

- Safe for multiple checks

However, hard inquiries are necessary when you actually apply for credit.

So the goal is:

👉 Minimize hard inquiries

👉 Maximize soft inquiries

Common Mistakes to Avoid

❌ Applying on Multiple Loan Apps

This leads to multiple hard inquiries

❌ Ignoring Credit Report

Not checking your report regularly is risky

❌ Applying Without Eligibility Check

Always check via soft inquiry first

❌ Panic Applications After Rejection

This worsens your situation

Read More: Why a CIBIL Score Below 650 Is Bad?

Expert Tips to Improve Loan Approval Chances

- Maintain CIBIL score above 750

- Keep credit utilization below 30%

- Avoid unnecessary inquiries

- Pay EMIs on time

- Use fewer loan apps

These tips will improve your loan approval chances significantly.

Conclusion

Understanding the difference between soft inquiry vs hard inquiry is crucial if you want to maintain a healthy credit profile and improve your loan approval chances.

While soft inquiries are completely safe, hard inquiries should be used carefully. Too many hard inquiries can reduce your credit score and signal risk to lenders.

The smart strategy is simple:

👉 Always start with a soft inquiry

👉 Apply only when you’re confident

👉 Avoid multiple applications

By following these steps, you can protect your CIBIL score, improve your financial profile, and increase your chances of getting approved for loans easily.

FAQs (Frequently Asked Questions)

1. What is the difference between soft and hard inquiry?

A soft inquiry does not affect your credit score, while a hard inquiry can reduce it slightly.

2. Does checking loan eligibility affect CIBIL score?

No, eligibility checks usually involve soft inquiries, which do not impact your score.

3. Does hard inquiry affect credit score?

Yes, a hard inquiry can reduce your credit score by a few points.

4. How many hard inquiries are too many?

More than 3–5 hard inquiries in a short period can negatively affect your loan approval chances.

5. Can multiple inquiries reduce loan approval chances?

Yes, multiple inquiries signal risk to lenders and may lead to rejection.

6. How to avoid hard inquiries on credit report?

Check eligibility first, apply selectively, and avoid multiple applications.