Why Personal Loan Gets Rejected? Real Reasons and Smart Fixes

Personal loans have become one of the fastest ways to arrange money in urgent situations. From handling medical bills to managing sudden expenses, they provide flexibility without requiring collateral. But despite the ease of application, many people still face rejection. This leads to a common concern: why personal loan gets rejected even after meeting basic requirements?

Table of Contents

ToggleThe truth is, lenders do not approve loans based only on income or documents. They analyze your entire financial behavior. Even a small weakness in your profile can affect the decision. That’s why understanding the deeper personal loan rejection reasons is essential before applying.

In this detailed guide, you will not only learn the causes behind rejection but also practical ways to improve your profile and increase your approval chances. This article is written in a natural, experience-based tone so you can actually apply these insights in real life.

How Banks Actually Decide Your Loan Approval

Most people think that submitting documents is enough to get a loan. In reality, banks use a combination of technology and risk analysis models to evaluate applicants. Your financial profile is scanned in seconds, and a decision is made based on multiple parameters.

These include your repayment track record, income consistency, credit utilization habits, and even how frequently you apply for credit. Every detail contributes to a risk score.

So if you are wondering why personal loan gets rejected, the answer lies in how your profile appears to the lender’s system — not just what you submit.

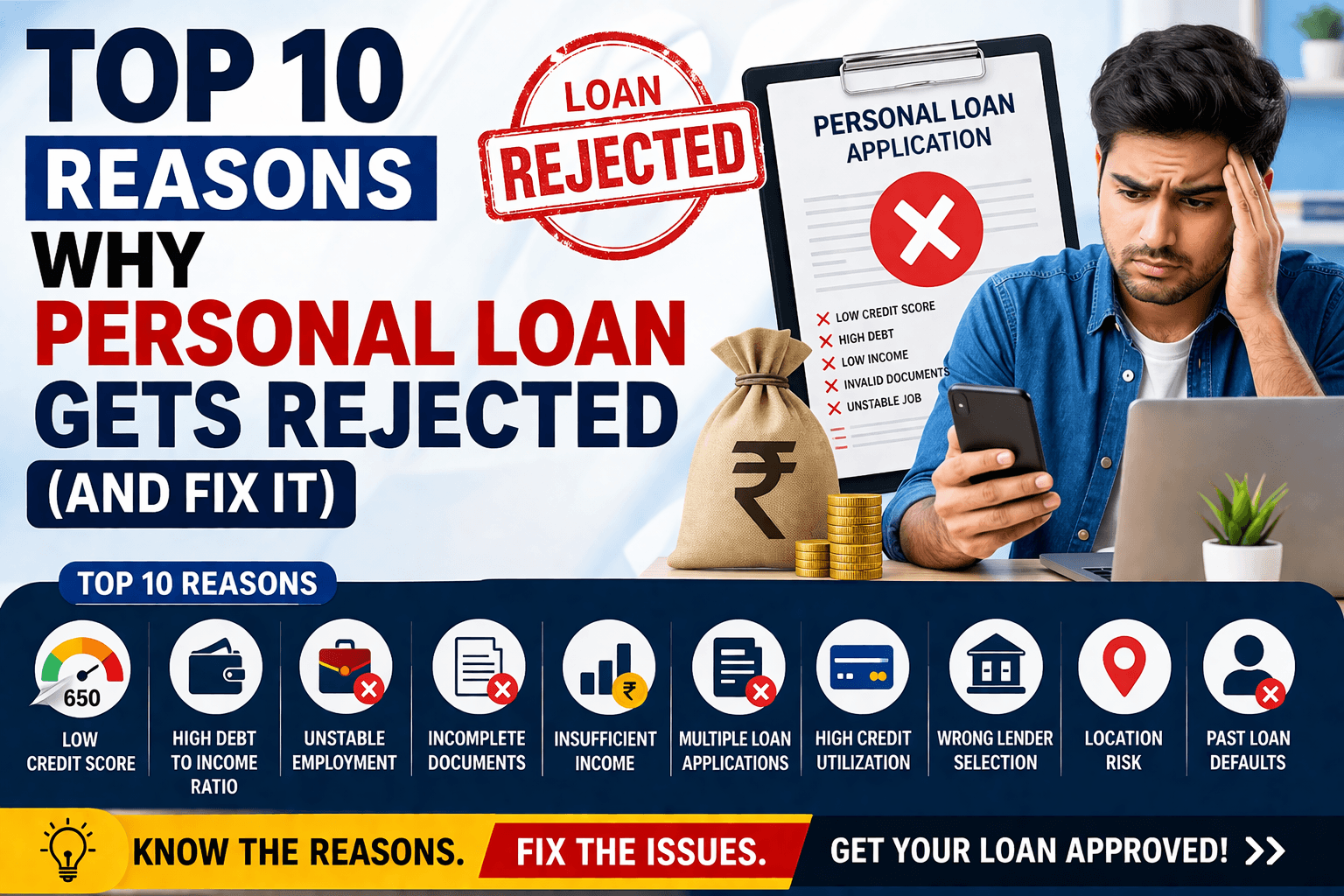

1. Weak Credit Profile

A fragile or poorly maintained credit profile is one of the strongest reasons behind rejection. Your credit score is more than just a number; it reflects your financial discipline over time.

If you have missed

payments in the past or carry high credit card balances, lenders may see you as a potential risk. Even if you have corrected your behavior recently, past patterns still matter.

To improve this, focus on consistency. Make every payment on time, keep your credit usage low, and avoid unnecessary borrowing. Over time, your score will gradually recover and strengthen your profile.

2. Income That Doesn’t Match the Loan Request

Another common issue arises when the loan amount does not align with your earnings. Lenders carefully evaluate whether your income can support the EMI comfortably.

If your requested amount seems too high compared to your salary, the system may automatically decline your application. This is not about your current ability but about long-term repayment sustainability.

A practical solution is to apply for a realistic loan amount. You can also strengthen your case by showing additional income sources or including a co-applicant.

3. Irregular Employment Pattern

Consistency in employment plays a bigger role than most applicants realize. If your work history shows frequent job switches or long gaps, lenders may question your income stability.

Even freelancers and self-employed individuals face this challenge if their income is not properly documented. From a lender’s perspective, predictability matters more than high but unstable earnings.

Maintaining a steady work record and providing clear income proof can help reduce this risk significantly.

4. Existing Financial Burden

If a large portion of your income is already committed to other financial obligations, lenders may hesitate to approve another loan. This is because your repayment capacity becomes limited.

Your financial commitments include not just loans but also credit card dues and other liabilities. When these exceed a certain level, your application may be flagged as risky.

Reducing your outstanding dues before applying can improve your chances. Even small improvements in your financial balance can make a noticeable difference.

5. Applying Too Frequently

Many applicants try their luck by submitting applications to multiple lenders at once. While this might seem like a smart approach, it often backfires.

Each application leaves a footprint on your credit report. When multiple requests appear within a short span, it signals financial stress to lenders.

Instead of rushing, take a more calculated approach. Evaluate your eligibility first and apply only where you have a higher probability of approval.

6. Errors in Personal or Financial Details

Sometimes, rejection happens not because of your financial profile but due to simple mistakes. Incorrect information, mismatched details, or missing documents can disrupt the verification process.

Even a small spelling difference in your name across documents can create complications. These issues may seem minor but can lead to rejection during automated checks.

Ensuring accuracy in every detail before submission is one of the easiest ways to avoid unnecessary rejection.

7. No Credit Activity

Having no borrowing history can also create problems. If you have never used credit before, lenders do not have enough data to evaluate your repayment behavior.

This situation makes it difficult for them to assess risk, which may result in rejection.

Starting with a small credit product and managing it responsibly can help build your profile. Over time, this creates a positive track record that improves your credibility.

8. Age-Related Limitations

Loan eligibility is often linked to your age group. Applicants at the very beginning or end of their earning years may face difficulties in getting approval.

Younger applicants may lack experience and income stability, while older individuals may have limited earning years left.

In such cases, applying with a co-applicant or choosing lenders with flexible policies can improve your chances.

9. Risk Perception Based on Location or Job Type

Certain locations and job categories are considered higher risk by lenders. This is based on historical data related to repayment patterns.

If your profile falls into such a category, your application may be scrutinized more strictly. This does not mean approval is impossible, but it does require a stronger overall profile.

Providing stable employment proof and maintaining consistent financial behavior can help offset this risk.

10. Negative Financial History

Your past financial behavior leaves a lasting impact. Defaults, settlements, or delayed payments can significantly affect your credibility.

Even if these issues occurred years ago, they may still influence the lender’s decision. This is one of the most critical personal loan rejection reasons.

Rebuilding trust takes time. Regular payments, disciplined credit usage, and patience are key to improving your financial image.

Practical Steps to Improve Your Approval Chances

Practical Steps to Improve Your Approval Chances

Once you understand why personal loan gets rejected, the next step is improvement. Instead of reapplying immediately, take time to strengthen your profile.

Start by reviewing your credit report and identifying weak areas. Focus on clearing dues, improving your score, and organizing your financial records.

Building a strong profile is not about quick fixes but about consistent habits. The more stable your financial behavior, the better your chances of approval.

Smart Approach Before Applying Again

Timing plays an important role in loan approval. Applying too soon after rejection can lead to another decline.

Give yourself time to correct the issues. Monitor your progress and apply only when you are confident about your eligibility.

Choosing the right lender is equally important. Not all lenders follow the same criteria, so finding one that aligns with your profile can increase your chances.

Conclusion

Understanding why personal loan gets rejected can save you from repeated failures and unnecessary stress. Loan rejection is not a dead end; it is a signal that your financial profile needs attention.

By making informed decisions and improving your financial habits, you can turn rejection into approval. Focus on long-term stability rather than short-term solutions.

With the right preparation, your next loan application can be successful and stress-free.

❓ Frequently Asked Questions (FAQs)

1. Why personal loan gets rejected even with a good salary?

A good salary alone does not guarantee approval. Lenders evaluate multiple factors such as your credit score, existing debts, repayment history, and job stability. If any of these areas are weak, your loan application may still be rejected despite having a decent income.

2. How can I check the exact reason for loan rejection?

You can request the lender or bank to provide the reason for rejection. In many cases, financial institutions share a general explanation. You can also review your credit report to identify issues like low score, high utilization, or missed payments.

3. Does loan rejection affect my CIBIL score?

Yes, indirectly. While rejection itself is not recorded, every loan application creates a hard inquiry on your credit report. Multiple inquiries within a short period can lower your credit score and reduce future approval chances.

4. How long should I wait before applying again after rejection?

It is advisable to wait at least 2 to 3 months before reapplying. During this time, you should work on improving your financial profile, such as increasing your credit score or reducing existing debts.

5. Can I get a personal loan after multiple rejections?

Yes, it is possible. However, you need to identify and fix the root cause first. Applying again without improving your profile will likely result in another rejection. Choosing the right lender based on your eligibility can also help.

6. What is the minimum credit score required for a personal loan?

Most lenders prefer a credit score of 700 or above. A score above 750 is considered strong and increases your chances of approval. Lower scores may still be accepted by some NBFCs but usually at higher interest rates.

7. Can I get a loan without a credit history?

Yes, but it can be challenging. Some lenders offer loans to first-time borrowers, but the approval criteria are stricter. Building a small credit history through credit cards or EMI products can improve your chances.

8. Does changing jobs frequently affect loan approval?

Yes, frequent job changes can create a negative impression. Lenders prefer applicants with stable employment, as it indicates consistent income. Staying in one job for a longer period can improve your credibility.

9. What should I do if my loan gets rejected due to low income?

You can apply for a smaller loan amount, add a co-applicant, or show additional income sources. Improving your income stability over time can also increase your eligibility.

10. Is it better to apply through a bank or a loan platform?

Both options have their advantages. Banks may offer lower interest rates but have stricter criteria. Loan platforms or NBFCs may provide easier approvals but sometimes at slightly higher rates. Choosing the right option depends on your financial profile.