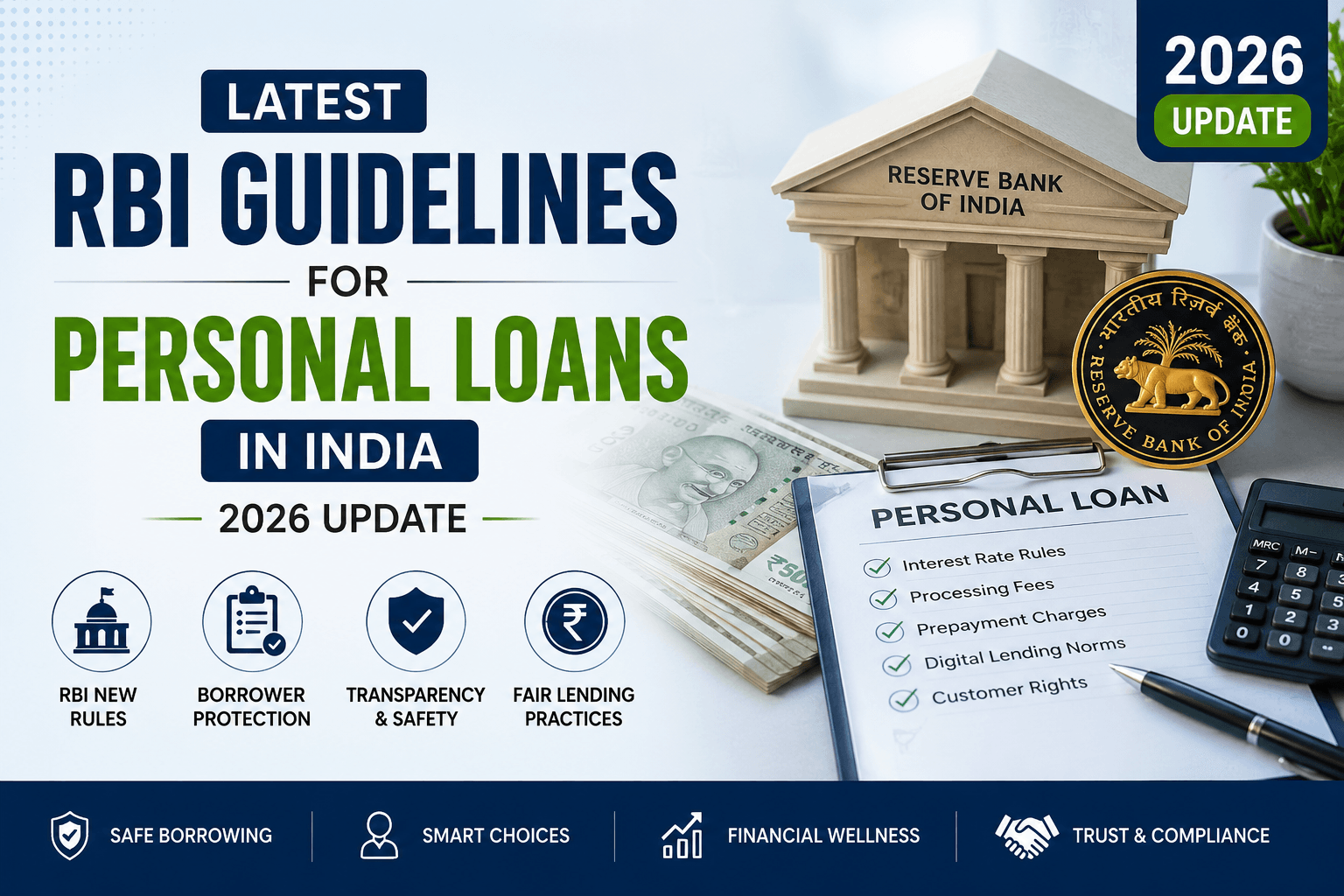

Latest RBI Guidelines for Personal Loans in India

If you’re planning to take a personal loan in 2026, understanding the RBI guidelines for personal loan 2026 is essential. These guidelines directly impact how loans are approved, how much you pay, what lenders can (and cannot) do, and how safe your data remains.

Table of Contents

ToggleThis comprehensive guide explains the latest RBI rules, digital lending norms, borrower rights, approval factors, and practical tips to help you make informed decisions.

What Are RBI Guidelines for Personal Loan 2026?

The RBI guidelines for personal loan 2026 are not a single new rulebook released in one go. Instead, they are a continuation and tightening of existing directions, especially those related to:

- Digital lending framework (strengthened since 2022)

- Transparency in loan pricing and charges

- Borrower data privacy and consent

- Fair lending practices and grievance redressal

- Responsible credit underwriting

In simple terms, RBI’s approach in 2026 focuses on three pillars:

1. Transparency – No hidden charges or misleading offers

2. Accountability – Lenders must clearly take responsibility

3. Borrower Protection – Data, dignity, and financial safety

Transparency & Protection is compulsory.

Key RBI Guidelines for Personal Loan 2026 (Core Regulatory Framework)

1. Mandatory Transparency in Loan Terms “RBI Guidelines”

One of the most important aspects of the RBI guidelines for personal loan 2026 is full disclosure before disbursement.

Lenders (banks and NBFCs) must clearly communicate:

- Annual Percentage Rate (APR)

- Processing fees and other charges

- EMI amount and tenure

- Total repayment obligation

- Prepayment or foreclosure charges

This information is typically shared through a Key Fact Statement (KFS)—a standardized document that summarizes the loan in simple terms.

👉 Why it matters: Borrowers can now compare loans easily and avoid hidden costs.

2. RBI Digital Lending Guidelines (Strengthened Framework)

The biggest regulatory shift in recent years—and still highly relevant in 2026—is RBI’s digital lending framework.

Under the current guidelines:

- Loans must be disbursed only by regulated entities (banks or RBI-registered NBFCs)

- Loan funds must be credited directly to the borrower’s bank account

- Third-party apps (Lending Service Providers) cannot act as independent lenders

👉 This eliminates the earlier confusion where many apps appeared to be lenders but were actually intermediaries.

3. RBI Guidelines for Direct Flow of Funds (No Pass-Through Accounts)

RBI has strictly mandated that:

- Loan disbursement must go directly from lender → borrower

- Repayment must go directly from borrower → lender

No third-party wallet, pool account, or intermediary routing is allowed.

👉 Impact:

- Reduces fraud risk

- Improves traceability

- Increases accountability

4. RBI Guidelines for Data Privacy and User Consent Rules

Under the RBI guidelines for personal loan 2026, data protection is a major focus.

Lenders and apps must:

- Collect only necessary data

- Take explicit user consent before accessing any data

- Avoid accessing:

- Contact lists

- Photo galleries

- Unrelated personal files

👉 Unauthorized data harvesting is a red flag—borrowers should avoid such apps.

5. RBI Guidelines for Cooling-Off Period (Exit Option for Borrowers)

A key borrower-friendly feature introduced in RBI’s framework is the cooling-off period.

- Borrowers can exit a loan within a specified time window

- Only minimal charges (if any) are applicable

👉 This gives borrowers a chance to reconsider decisions made under urgency or pressure.

6. RBI Guidelines for Clear Identification of the Lender

RBI requires that borrowers must always know:

- Who the actual lender is (bank/NBFC name)

- Who is acting as the service provider (app/platform)

👉 No ambiguity is allowed. If the lender is not clearly disclosed, it’s a major compliance issue.

7. RBI Guidelines for Fair Lending and Non-Coercive Recovery Practices

RBI has reinforced rules against harassment and unethical recovery:

- Recovery agents must follow fair conduct guidelines

- No threats, public shaming, or misuse of personal data

- Borrowers must have access to a grievance redressal system

👉 This is especially important given past complaints against some digital loan apps.

Read More: What Happens If You Don’t Repay Loan

RBI Guidelines for Personal Loan 2026 and Their Impact on Borrowers

The updated regulatory environment has significantly changed how personal loans work in India.

1. Safer Borrowing Environment

- Fraudulent apps are being filtered out

- Only regulated lenders dominate the market

- Better legal protection for borrowers

2. More Structured Loan Approval

Loan approvals are now more:

- Data-driven

- Risk-based

- Transparent

Lenders focus heavily on:

- Credit score

- Income consistency

- Existing liabilities

3. Reduced Hidden Costs

Because of mandatory disclosures:

- Borrowers can compare total loan cost

- Misleading “low EMI” marketing is less effective

- APR-based comparison improves decision-making

4. Better Borrower Awareness

With RBI’s push for transparency:

- Borrowers are more informed

- Loan literacy is increasing

- Financial decisions are becoming more rational

RBI Rules for Instant Loan Apps in 2026

Instant loan apps are still popular, but under strict regulatory oversight.

According to the RBI guidelines for personal loan 2026:

- Every app must be linked to a regulated lender

- The loan agreement must be provided to the borrower

- All charges must be disclosed upfront

- Apps cannot misuse borrower data

👉 If an app promises “instant loan without documents and without lender disclosure,” it is likely risky.

How RBI Guidelines Affect Loan Approval Chances

The RBI personal loan rules India 2026 indirectly influence approval in several ways:

1. Higher Importance of Credit Score

- Score above 700 improves approval chances

- Low score leads to stricter scrutiny

2. Debt-to-Income Ratio Matters

- High existing EMIs reduce eligibility

- Lenders prefer balanced financial profiles

3. Income Stability is Crucial

- Salaried individuals with stable jobs are preferred

- Self-employed borrowers need strong financial records

Common Reasons for Loan Rejection Under RBI Framework

While RBI does not directly reject loans, its framework encourages stricter evaluation.

Common reasons include:

- Low credit score

- High existing debt

- Irregular income

- Incomplete documentation

- Mismatch in personal or financial details

Read More: Fast Approved Personal Loan in 2026

How to Improve Approval Chances (RBI-Aligned Strategy)

To align with the RBI guidelines for personal loan 2026, borrowers should:

- Maintain a healthy credit score (700+)

- Keep EMIs below 40–50% of income

- Avoid multiple loan applications simultaneously

- Submit accurate and complete documents

- Build a stable income history

Documents Required for Personal Loan (As per Standard Practice)

While RBI does not prescribe a fixed list, most lenders require:

- Identity proof (Aadhaar/PAN)

- Address proof

- Income proof (salary slips or ITR)

- Bank statements

👉 Documentation standards are more uniform now due to regulatory alignment.

RBI Guidelines for NBFC Personal Loans

Non-Banking Financial Companies (NBFCs) are also governed by RBI.

Under the RBI guidelines for personal loan 2026:

- NBFCs must follow the same transparency norms

- Digital lending rules apply equally

- Borrower protection standards are identical

👉 This means NBFC loans can be safe if the entity is RBI-registered.

Mistakes to Avoid When Taking a Personal Loan in 2026

Even with strong regulations, borrowers must stay cautious.

Avoid:

- Ignoring the Key Fact Statement

- Choosing lenders based only on quick approval

- Falling for “zero documentation” claims

- Sharing unnecessary personal data

- Taking multiple loans simultaneously

Read More: Best Instant Personal Loan Apps in India

Why RBI Guidelines Matter More Than Ever in 2026

The lending market has changed:

- Rapid growth of fintech platforms

- Increased digital loan adoption

- Past rise in fraudulent lending apps

RBI’s response has been to:

- Tighten regulations

- Standardize processes

- Protect borrowers

👉 Result: A more secure, transparent, and trustworthy lending ecosystem

Conclusion

The RBI guidelines for personal loan 2026 have significantly improved the lending environment in India. Borrowers today benefit from:

- Greater transparency

- Stronger data protection

- Fairer lending practices

- Reduced fraud risk

However, regulations alone are not enough. Smart borrowing decisions—combined with awareness of RBI rules—are the key to getting the best loan deal.

If you understand these guidelines and apply strategically, you can increase your approval chances, reduce costs, and avoid financial mistakes.

FAQs – RBI Guidelines for Personal Loan 2026

Q1. What are RBI guidelines for personal loan 2026?

They are regulatory directions focusing on transparency, digital lending control, borrower protection, and fair lending practices.

Q2. Are instant loan apps safe in India?

Only if they are connected to an RBI-regulated bank or NBFC and follow official guidelines.

Q3. Can I cancel a loan after approval?

Yes, under the cooling-off period, borrowers can exit within a specified time.

Q4. Does RBI fix personal loan interest rates?

No, but it ensures transparency and fair practices in pricing.

Q5. What is the biggest change in recent RBI rules?

The digital lending framework—especially rules around data privacy, fund flow, and lender accountability.