How to Increase CIBIL Score Fast in India

If you’ve ever been rejected for a loan or offered a high interest rate, your credit profile is likely the reason. This is where most people start searching how to increase CIBIL score, but they often find repetitive and surface-level advice.

Table of Contents

ToggleThis guide takes a different approach. Instead of generic tips, you’ll learn practical, behavior-based methods that actually help improve your score over time—making you a more trustworthy borrower in the eyes of lenders.

What is a CIBIL Score and Why It Matters

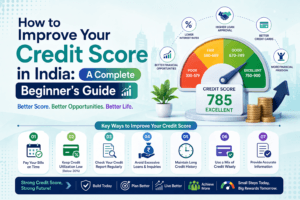

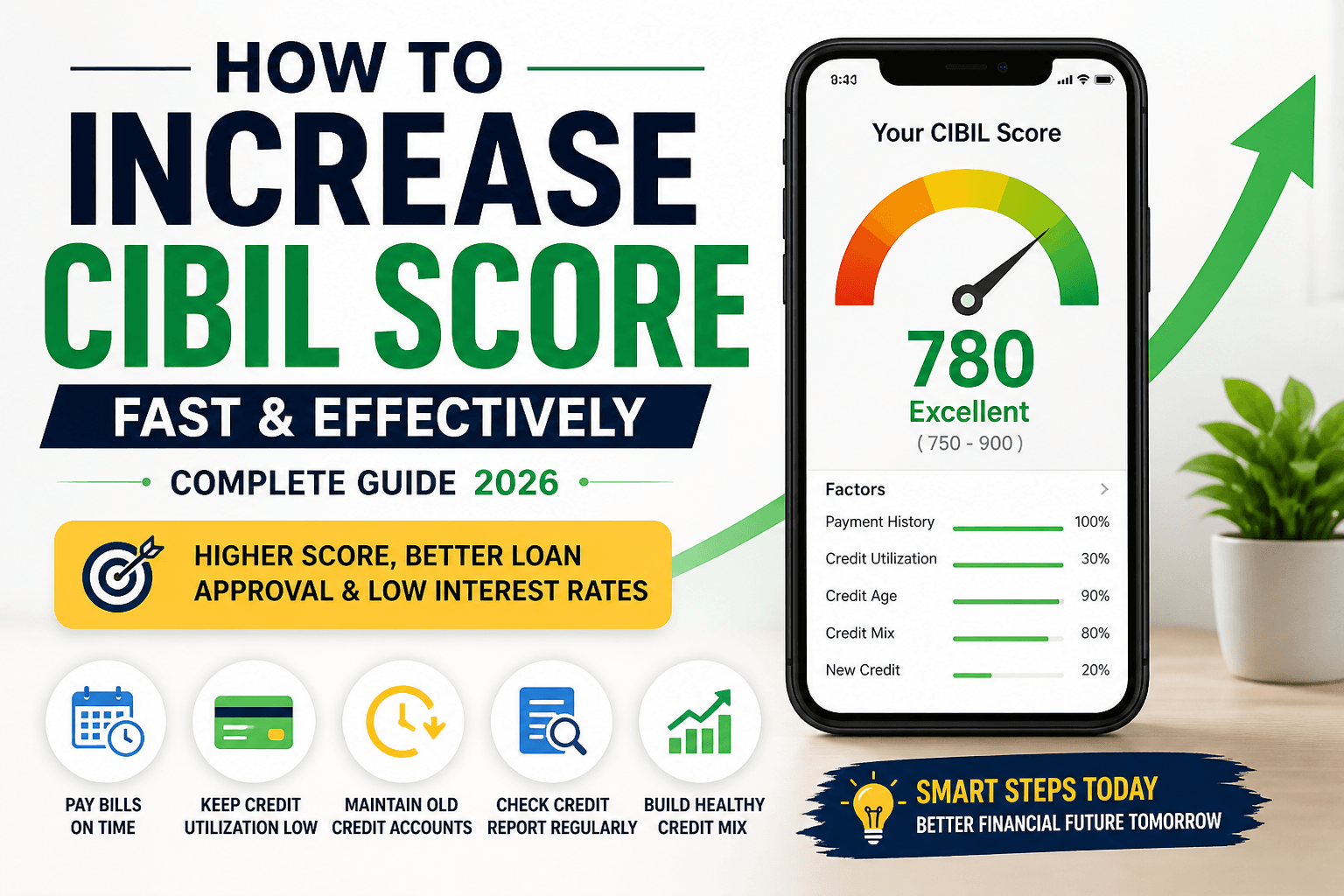

A CIBIL score is a three-digit number (300–900) that reflects how responsibly you manage borrowed money.

- 750+ → Strong and reliable profile

- 650–749 → Acceptable but not ideal

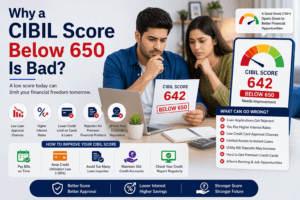

- Below 650 → Risky from a lender’s perspective

A higher score doesn’t just improve approval chances—it also reduces borrowing costs.

Common Reasons Your Score Drops

Before learning how to increase CIBIL score, it’s important to understand what causes the decline:

- Irregular or delayed payments

- High dependence on credit cards

- Frequent loan or card applications

- Settled accounts instead of fully closed loans

- Limited or inactive credit history

- Errors in your credit report

Identifying these patterns is the first step toward fixing them.

Read More: Soft Inquiry vs Hard Inquiry

How to Increase CIBIL Score Step by Step

1. How to Increase CIBIL Score by Building Payment Consistency

Your repayment pattern is the backbone of your credit profile. Even a small delay can leave a negative mark. Instead of paying on the due date, try paying a few days early. This creates a buffer and builds a habit of consistency.

2. How to Increase CIBIL Score by Controlling Credit Usage

Using too much of your available credit signals financial pressure. A safer approach is to keep your usage below 30% of your limit. This shows that you are not dependent on borrowed money for daily expenses.

3. How to Increase CIBIL Score by Preserving Old Credit Accounts

Older accounts act like a financial track record. Closing them too early reduces your credit history length, which can weaken your overall profile. Keeping them active—even with minimal usage—adds stability.

4. How to Increase CIBIL Score Using Secured Credit Options

If your score is low or you have no credit history, starting with unsecured loans can be difficult. A smarter entry point is a secured credit card backed by a fixed deposit. It allows you to build a positive record without high risk.

5. How to Increase CIBIL Score by Avoiding Loan Settlements

Many borrowers choose settlement to clear dues quickly, but this creates a negative impression. A “closed” loan shows responsibility, while a “settled” loan suggests inability to repay fully. Always aim for complete closure whenever possible.

6. How to Increase CIBIL Score by Reducing Unnecessary Applications

Each time you apply for credit, it leaves a trace on your report. Applying too frequently makes lenders cautious. Instead, plan your applications and avoid multiple requests within a short period.

7. How to Increase CIBIL Score by Reviewing Your Credit Report

Credit reports are not always error-free. Incorrect entries, duplicate accounts, or outdated defaults can lower your score. Regularly checking your report and correcting mistakes can lead to quick improvements.

How Long Does It Take to Increase CIBIL Score?

Improving your score is gradual but predictable:

- First 30–45 days → Initial correction

- 2–3 months → Noticeable improvement

- 6 months or more → Strong, stable score

Consistency matters more than speed.

Fast-Track Methods to Increase CIBIL Score

If you want to accelerate progress:

- Clear outstanding balances completely

- Reduce your credit card usage immediately

- Avoid new credit unless necessary

- Maintain a perfect payment record

These actions create quick positive signals in your credit profile.

Read More: Why a CIBIL Score Below 650 Is Bad?

Mistakes That Prevent You from Increasing CIBIL Score

Some habits silently damage your progress:

- Paying only the minimum due

- Using your full credit limit regularly

- Ignoring small overdue amounts

- Applying for multiple loans at once

- Not monitoring your credit report

Avoiding these mistakes is just as important as following the right steps.

Benefits of Increasing Your CIBIL Score

A strong credit score improves your financial flexibility:

- Faster loan approvals

- Lower interest rates

- Higher credit limits

- Better financial offers

It essentially makes borrowing easier and more affordable.

A Practical Example

Consider a borrower with a score around 580.

By focusing on:

- Timely payments

- Reduced credit usage

- Limited applications

The score improved to above 730 within six months.

No shortcuts—just consistent financial discipline.

Conclusion

If you’re serious about learning how to increase CIBIL score, the key lies in your daily financial behavior. There is no instant fix, but with the right habits:

- Pay on time

- Use credit carefully

- Avoid unnecessary risk

Your score will gradually reflect your improved discipline. Small actions like reducing outstanding balances and limiting new credit applications can create a noticeable impact over time. Consistency in managing your finances builds trust in your credit profile, which lenders value the most.

Even minor improvements in your habits can lead to significant changes in your score over a few months. Staying aware of your credit report and correcting errors further strengthens your financial position. Ultimately, a disciplined approach today ensures better loan opportunities and financial flexibility in the future.

FAQs Of (How To Increase CIBIL Score)

Q1. How to increase CIBIL score quickly?

Focus on timely payments, low credit utilization, and avoiding unnecessary applications.

Q2. Can a score below 600 be improved?

Yes, with consistent repayment behavior and controlled credit usage.

Q3. Does checking my own score affect it?

No, self-checks do not impact your credit score.

Q4. How often should I review my credit report?

At least once every few months to catch errors early.

Q5. How long does it take to increase CIBIL score?

It usually takes 1 to 3 months to see initial improvement and 6 months or more for significant growth, depending on your financial habits.

Q6. What is the minimum CIBIL score required for a personal loan?

Most lenders prefer a score of 700 or above, but some NBFCs may approve loans even with lower scores at higher interest rates.

Q7. Can paying only the minimum due improve my CIBIL score?

No, paying only the minimum due does not help much. You should always try to pay the full outstanding amount to improve your score.

Q8. Does closing a credit card increase CIBIL score?

Not always. Closing old credit cards can reduce your credit history length and may negatively affect your score.

Q9. Can I increase my CIBIL score without taking a loan?

Yes, you can use a credit card responsibly, maintain low utilization, and pay bills on time to improve your score without taking a loan.

Q10. Does increasing my credit limit help improve my CIBIL score?

Yes, increasing your credit limit can improve your CIBIL score if your spending remains the same, as it lowers your credit utilization ratio.