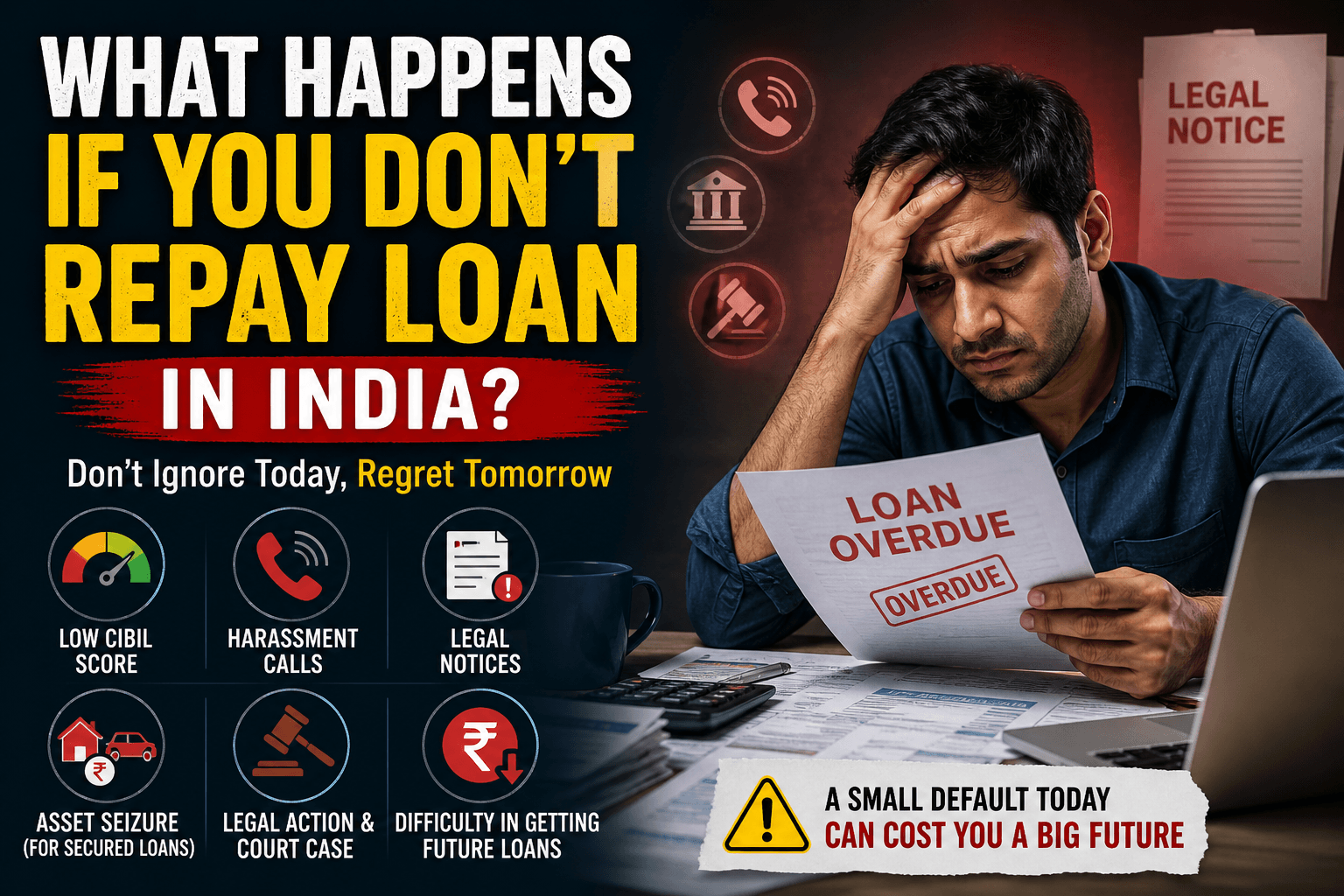

What Happens If You Don’t Repay Loan in India?

Taking a loan can be a smart financial move when used correctly. But what happens if things don’t go as planned and you fail to repay your loan? Many people ignore this question until they face the situation themselves.

Table of Contents

ToggleIn this detailed, we will explain what happens if you don’t repay loan in India, covering penalties, credit score impact, legal action, and practical solutions to avoid serious consequences.

Understanding Loan Repayment in India

Before diving into consequences, it’s important to understand how loan repayment works.

When you take a loan:

- You agree to repay via EMIs (Equated Monthly Installments)

- Each EMI includes principal + interest

- Payment must be made on a fixed due date

Missing even a single EMI can trigger penalties and impact your financial profile.

What Happens If You Don’t Repay Loan in India? (Step-by-Step Impact)

1. Late Payment Charges after Miss EMI

The first consequence is financial penalties.

If you miss your EMI:

- Late payment fee is charged

- Penal interest is added (2%–4% extra)

- GST is applied on penalties

Over time, your total loan burden increases significantly.

👉 Example:

A ₹10,000 EMI missed for 3 months can turn into ₹11,500+ due to penalties.

2. Bad Impact on CIBIL Score

One of the biggest impacts of loan default is on your credit score.

Your repayment behavior is reported to credit bureaus like:

- TransUnion CIBIL

- Experian

If you don’t repay:

- Your score drops quickly

- Late payments are recorded

- Default status is marked

👉 Ideal score: 750+

👉 Risky score: Below 650

A low score makes future loans almost impossible.

3. Continuous Recovery Calls and Follow-ups

After missing EMIs, banks start recovery actions:

- Phone calls

- SMS reminders

- Email notices

- WhatsApp alerts

If you ignore them:

- Recovery agents may visit your home

- Pressure increases gradually

Important: Recovery agents must follow RBI guidelines and cannot harass you illegally.

4. Loan Account Becomes NPA (Non-Performing Asset)

If you don’t pay EMI for 90 days:

➡️ Your loan becomes an NPA (Non-Performing Asset)

This means:

- Bank treats your loan as default

- Recovery process becomes aggressive

- Your credit profile gets severely damaged

This is a serious stage where financial institutions lose trust in you.

5. Legal Notice and Court Case

If the loan remains unpaid:

- Legal notice is issued

- Case can be filed in court

- Bank may approach Debt Recovery Tribunal (DRT)

Legal action depends on:

- Loan amount

- Type of loan

- Duration of default

Ignoring legal notices can worsen your situation.

6. Asset Seizure in Secured Loans

If your loan is secured (backed by asset), the lender can take your asset.

Examples:

- Home Loan → Property auction

- Car Loan → Vehicle repossession

- Gold Loan → Gold auction

This is done under laws like: SARFAESI Act 2002

Under this law, banks can recover money without court intervention in many cases.

7. Future Loan Approval Almost Impossible

Loan default creates long-term financial problems:

- Loan rejection

- Higher interest rates

- Strict documentation

- Low credit limits

Even NBFCs and apps may reject your application.

8. Loan Settlement Ka Negative Impact

If you cannot repay, banks may offer settlement.

But:

- Loan is marked as “Settled”

- Not equal to “Closed”

- Remains in credit report for years

This affects your credibility.

9. Mental Stress and Financial Pressure

Ignoring loan repayment doesn’t just affect money—it affects your life.

You may face:

- Constant stress

- Anxiety from recovery calls

- Family pressure

- Loss of financial confidence

This is why timely action is very important.

Common Reasons Why People Don’t Repay Loans

Understanding the reasons can help avoid mistakes:

- Job loss

- Medical emergency

- Poor financial planning

- Multiple loans at once

- Overuse of credit cards

What to Do If You Cannot Repay Loan in India?

1. Contact Your Bank Immediately

Talk to your lender and explain your situation.

Banks may offer:

- EMI restructuring

- Tenure extension

- Temporary relief

2. Opt for Loan Restructuring

Restructuring helps:

- Reduce EMI burden

- Increase repayment time

- Avoid default status

3. Balance Transfer Option

You can transfer your loan to another bank with:

- Lower interest rate

- Better EMI structure

4. Convert Credit Card Dues into EMI

This reduces:

- Interest burden

- Monthly pressure

5. Avoid Multiple Loans

Taking too many loans increases risk of default.

Always calculate:

- Monthly income

- EMI capacity (ideally < 40% of income)

What Happens If You Don’t Repay Loan in India – Long-Term Financial Impact

Understanding what happens if you don’t repay loan in India is not just about immediate penalties—it also affects your long-term financial stability.

If you continue to ignore your loan repayment:

- Your credit history remains negative for years

- Banks and NBFCs mark you as a high-risk borrower

- You may face difficulty in renting a house or getting approval for financial services

- Even job opportunities in some financial sectors can be affected

Over time, rebuilding trust with lenders becomes very difficult. Even if you clear the loan later, your past record stays in your credit report for several years.

👉 Example:

If you default on a loan today, its impact can remain visible in your credit profile for up to 7 years.

Key Takeaway:

What happens if you don’t repay loan in India is not just a short-term problem—it can damage your financial future for many years. Acting early and responsibly is always the best solution.

Smart Tips to Avoid Loan Default

- Pay EMIs on time

- Set auto-debit from bank account

- Maintain emergency fund (3–6 months expenses)

- Track your credit score regularly

- Borrow only what you can repay

Real-Life Example (What Happens If You Don’t Repay Loan in India?)

Rahul took a personal loan of ₹2 lakh. After losing his job, he missed EMIs for 4 months.

Result:

- His CIBIL score dropped from 750 to 610

- Bank sent legal notice

- Recovery calls increased

- Future loan applications got rejected

Later, he opted for restructuring and slowly improved his score.

👉 Lesson: Early action saves you from bigger problems.

Conclusion

What happens if you don’t repay loan in India is not just about penalties—it’s a chain reaction of financial, legal, and emotional problems.

From:

- Late fees

- CIBIL score damage

- Recovery pressure

- Legal action

- Asset loss

Everything can escalate quickly if ignored.

👉 The smartest move is simple:

Communicate early, plan smartly, and never ignore your EMIs.

FAQs – What Happens If You Don’t Repay Loan in India

1. Can you go to jail for not repaying a loan in India?

No, loan default is generally a civil matter, not a criminal offense. Jail can happen only in cases involving fraud or intentional cheating.

2. After how many days can legal action start?

Legal action can usually begin after 90+ days of non-payment, when the loan is classified as a default (NPA).

3. Can the bank visit your home?

Yes, recovery agents can visit your home, but they must follow proper legal guidelines and cannot harass or threaten you.

4. Is loan settlement a good option?

Loan settlement should be considered as a last resort. It negatively affects your credit score and future loan eligibility.

5. How long does it take to improve a CIBIL score?

With regular and timely repayments, your CIBIL score can start improving within 6–12 months.