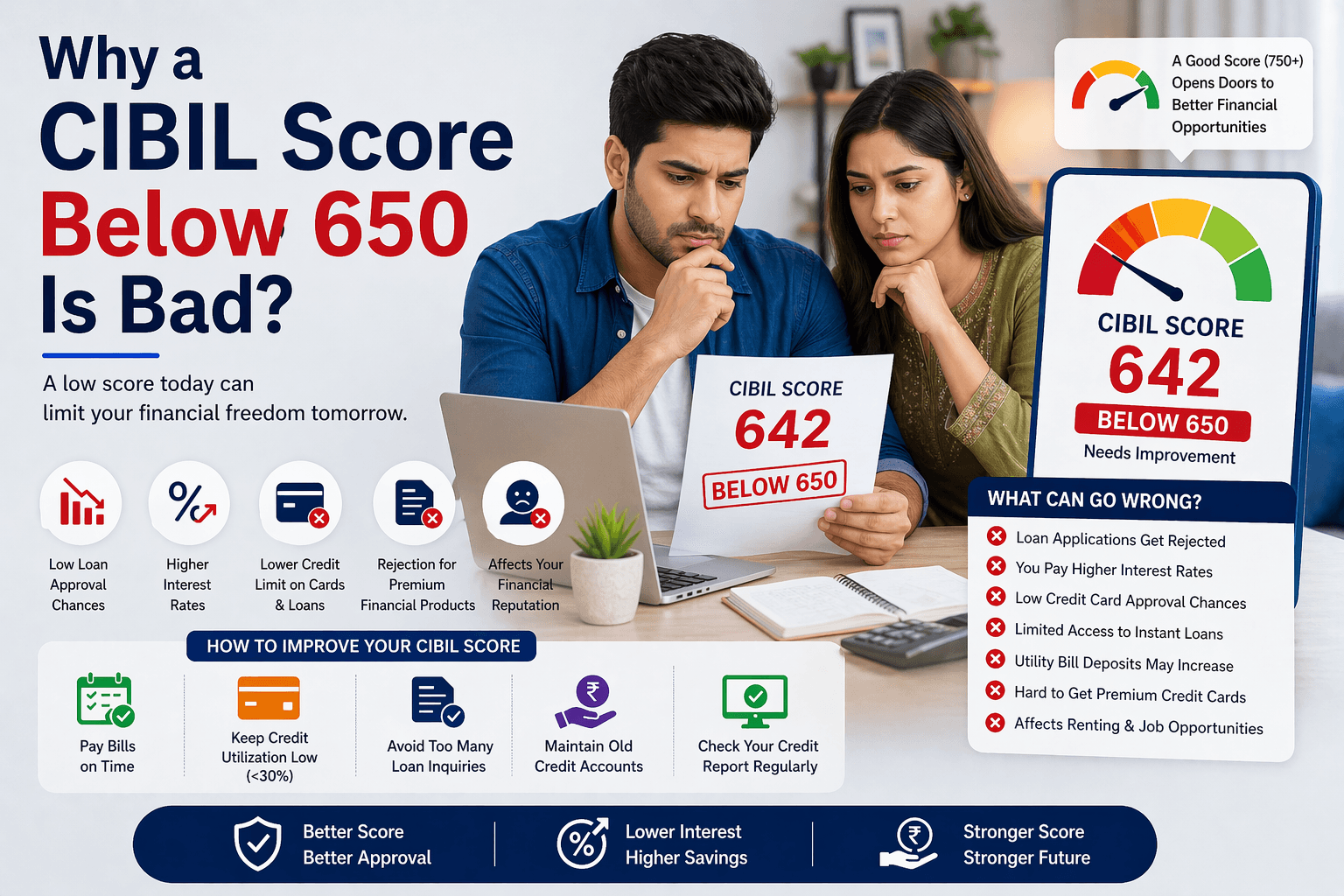

Why a CIBIL Score Below 650 Is Bad

A CIBIL score plays a very important role in your financial life, especially today, when almost every major financial decision depends on your credit profile.

Table of Contents

ToggleWhether you are planning to take a personal loan, home loan, car loan, or even apply for a credit card, your CIBIL score is one of the first things banks and financial institutions check.

It acts like a financial report card, showing lenders how responsible you are in managing credit. A high score indicates that you are a reliable borrower who pays back loans on time, while a low score may make banks and NBFCs cautious about your creditworthiness.

Additionally, your CIBIL score also determines how much loan you can get, what interest rate you will be offered, and how quickly your loan will be approved. Therefore, it is not just a number but a key indicator of your overall financial health. By making timely payments and using credit responsibly, you can improve your score, which can help you access lower interest rates and easier credit facilities in the future.

What is a CIBIL Score?

A CIBIL score is a three-digit number that represents your creditworthiness. It shows how responsible you are in managing loans and credit cards. Lenders use it to decide your loan approval, interest rates, and credit eligibility.

750 – 900 → Excellent 👍

700 – 749 → Good 🙂

650 – 699 → Average 😐

Below 650 → Poor ❌

👉 So, a score of 650 falls in the “average” category

Is a CIBIL Score of 650 Good or Bad?

A 650 CIBIL score is neither very good nor very bad — it is considered average.

Good Side:

- You may still get loans approved

- Some NBFCs may offer credit

Credit card - approval possible (limited options)

Bad Side:

- Banks may hesitate to approve loans

- Interest rates can be higher

- Loan amount may be lower

- Limited credit card options

👉 So overall, 650 is not ideal if you want easy and cheap loans.

Loan Approval with 650 CIBIL Score

If your score is around 650, you might be wondering how it affects your chances of getting loans or credit cards. Here’s what you can typically expect:

Personal Loan: Approval is possible, but interest rates may be higher.

Home Loan: Approval may be difficult, but not impossible.

Credit Card: Mostly basic cards with limited features are available.

💡 Tip: Banks generally prefer a score of 700+, so a 650 CIBIL score is considered a medium-risk profile.

Why 650 CIBIL Score is Considered Risky

A CIBIL score of 650 is generally considered average, and lenders often view it with caution. While it is not a “bad” score, it does indicate some level of financial risk. But why exactly is 650 seen as risky? Let’s break it down:

1. Missed or Late EMIs

Lenders carefully check your repayment history. Even a few missed or late EMIs can lower your score. A 650 score often signals that there may have been delays in repayment in the past. This raises concerns about your ability to repay future loans on time.

2. High Credit Utilization

Credit utilization is the ratio of your credit card balance to your credit limit. If your utilization is consistently high (above 30–40%), lenders may think you rely heavily on borrowed money. A 650 score may indicate over-dependence on credit, which is considered risky.

3. Limited or Short Credit History

A 650 score can also result from limited or short credit history. Lenders prefer borrowers with long-standing accounts because it provides more proof of responsible credit behavior. If your credit history is short, even timely payments may not fully reflect your reliability.

4. Multiple Loan or Credit Inquiries

Frequent applications for loans or credit cards can generate hard inquiries on your credit report. Too many inquiries in a short time can reduce your score and signal financial stress or high credit demand, which lenders interpret as risky.

Impact on Loan Approval and Interest Rates due to these factors, lenders may:

- Offer smaller loan amounts.

- Charge higher interest rates.

- Apply stricter terms and conditions.

💡 Tip: While 650 is risky compared to 700+, it is not a barrier. With responsible credit behavior, timely payments, and low credit utilization, you can gradually improve your score and reduce perceived risk.

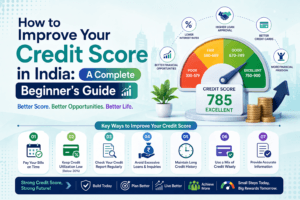

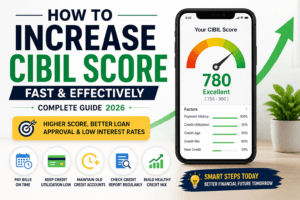

How to Improve Your CIBIL Score from 650

If your CIBIL score is around 650, there’s no need to worry. While it is considered an average score, with the right financial habits, you can gradually improve it and unlock better loan and credit opportunities. Here are the key steps to boost your CIBIL score:

1. Pay EMIs and Bills on Time

Late payments are one of the biggest reasons for a low CIBIL score. Whether it’s a personal loan, home loan, or credit card bill, ensure that you pay on or before the due date. Even missing one EMI can slightly lower your score, while consistently paying on time over months will gradually increase it.

💡 Pro Tip: Set up auto-debit or reminders to never miss a payment.

2. Reduce Credit Card Usage

Your credit utilization ratio—the percentage of your credit limit that you use—affects your score significantly. Experts recommend keeping your usage below 30% of your total credit limit. High utilization signals to lenders that you may be financially stressed.

For example, if your card limit is ₹50,000, try not to carry a balance above ₹15,000 at any time. Lower utilization shows responsible credit behavior and helps increase your score.

3. Avoid Multiple Loan or Credit Applications

Applying for several loans or credit cards in a short span creates hard inquiries on your credit report. Each hard inquiry can slightly reduce your score and signal to lenders that you might be over-reliant on credit.

💡 Pro Tip: Only apply for credit when necessary, and space out applications by a few months.

4. Maintain Old Credit Accounts

Length of credit history matters. Older accounts indicate financial stability and responsible credit usage. Avoid closing old credit cards or accounts, even if you don’t use them regularly, as they contribute positively to your credit history and score.

5. Check Your CIBIL Report Regularly

Errors in your CIBIL report can unfairly lower your score. Common errors include wrong payment status, duplicated accounts, or incorrect personal information.

Make it a habit to check your credit report at least once a year, and immediately raise corrections if you find discrepancies.

Additional Tips to Boost Your Score

- Diversify your credit mix: Having a combination of secured loans (like a home loan) and unsecured credit (like personal loans or credit cards) can improve your score.

- Pay more than the minimum due: On credit cards, paying the full outstanding balance is ideal. Paying only the minimum keeps utilization high, which slows score improvement.

- Keep EMIs affordable: Avoid taking loans that strain your monthly budget, as delayed or missed payments hurt your score.

💡 Key Takeaway: Improving your CIBIL score is a gradual process. With consistent effort, a score of 650 can reach 700+ within 3–6 months, and with more disciplined financial behavior, it can go above 750 in 6–12 months.

How Long Does It Take to Improve Score?

If you follow the proper steps consistently, you can see noticeable improvements in your score over time. It’s important to remember that credit score improvement is gradual, and there are no instant fixes.

650 → 700+ in 3 to 6 months

650 → 750+ in 6 to 12 months

Consistency is key: Regularly paying EMIs on time, maintaining low credit utilization, and avoiding multiple loan applications will steadily increase your score. The more disciplined you are, the faster your CIBIL score improves.

Conclusion

A CIBIL score of 650 sits in the average range, meaning it’s not a deal-breaker, but it can limit your financial options.

With this score, you can still get loans or credit cards, but expect higher interest rates, lower loan amounts, and stricter approval conditions. It’s a score that signals to lenders that you are somewhat reliable but may carry moderate risk.

For practical financial planning, here’s what you can do:

- Prioritize timely payments: Start with any pending EMIs or credit card bills to avoid further dips.

- Plan your borrowings wisely: Only apply for loans or cards you truly need, rather than multiple products at once.

- Maintain low credit utilization: Keeping usage below 30% not only helps improve your score but also shows financial discipline.

- Monitor and correct errors: Regularly check your CIBIL report to ensure there are no mistakes dragging your score down.

By following these practical steps, you can gradually raise your score to 700+ in a few months and eventually aim for 750+, which lenders consider strong and reliable. A higher score means better interest rates, faster approvals, higher loan limits, and more premium credit card options.

Takeaway: Don’t panic over a 650 score—focus on consistent financial habits, and over time, your creditworthiness will improve, opening doors to smarter and cheaper financial opportunities.