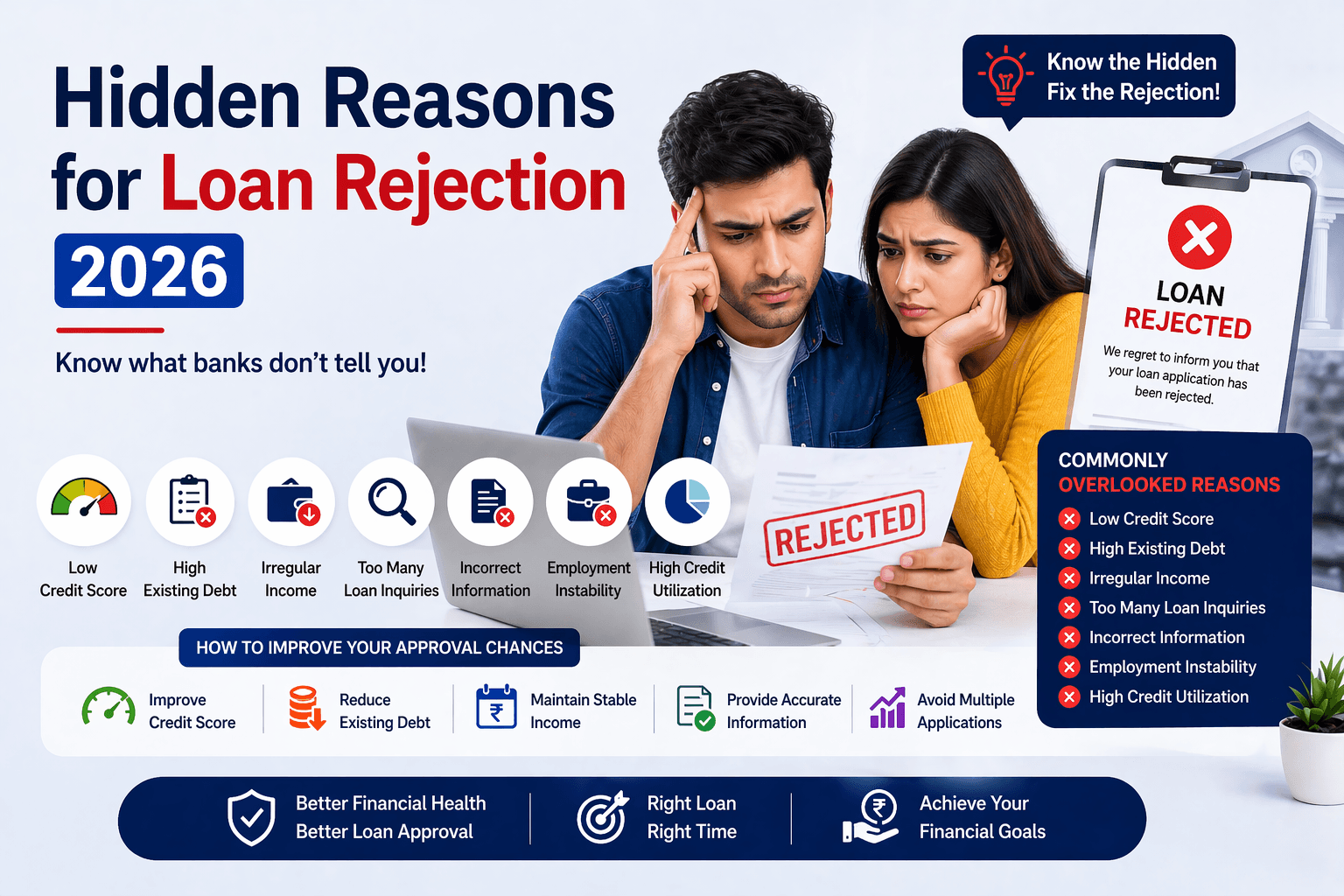

Hidden Reasons for Loan Rejection

In today’s fast-growing financial ecosystem, applying for a loan has become extremely easy. With just a few clicks, you can submit your application and expect quick approval. However, what most people don’t understand is that loan approval has become more complex behind the scenes.

Table of Contents

ToggleBanks and NBFCs in 2026 are no longer relying only on basic factors like income or credit score. Instead, they use advanced risk analysis systems, AI-based profiling, and behavioral tracking to evaluate applicants.

This is the reason why:

- People with decent income still get rejected

- Applicants with good credit scores face issues

- Even repeat borrowers struggle with approvals

👉 The truth is simple:

Loan rejection today is driven by hidden financial signals that most applicants ignore.

In this comprehensive guide, we will break down these hidden reasons in depth, so you can not only understand them but also take practical steps to fix them.

1. Behavioral Banking Analysis: The Silent Decision Maker

Most applicants think that banks only check income and documents. But in reality, your bank statement is deeply analyzed.

What Banks Actually Check:

- Daily balance patterns

- Spending habits

- Cash withdrawals vs digital transactions

- Stability of income credits

Hidden Red Flags:

- Sudden spikes in income (non-regular credits)

- Frequent low balance situations

- Heavy cash withdrawals

- Irregular salary dates

👉 These patterns indicate financial instability, even if your income looks good on paper.

How to Fix It:

- Maintain a stable average balance

- Avoid unnecessary cash transactions

- Keep salary credits consistent

- Show disciplined spending behavior

2. Credit Score vs Credit Behavior (Big Difference)

Many people believe that a 700+ credit score guarantees approval. But that’s not entirely true.

Hidden Reality:

Banks look beyond the score into your credit behavior, such as:

- How often you use your credit

- How quickly you repay

- Your dependency on loans

- Common Mistakes:

- Using 80–90% of credit card limit

- Paying only minimum dues

- Frequently taking short-term loans

👉 Even with a good score, these habits make you a high-risk borrower.

Best Practice:

- Keep credit utilization below 30%

- Pay full dues on time

- Avoid unnecessary borrowing

3. FOIR (Fixed Obligation to Income Ratio) – The Real Game Changer

FOIR is one of the most important yet least understood factors.

👉 It measures how much of your income is already committed to EMIs.

Example:

- Monthly income: ₹60,000

- Existing EMIs: ₹30,000

- FOIR = 50%

Most lenders prefer FOIR below 40–50%.

Hidden Issue:

Even if your income is high, high obligations reduce your eligibility.

Solution:

- Close small loans before applying

- Avoid taking multiple EMIs

- Increase declared income (if possible)

4. Employment Stability & Career Risk Analysis

In 2026, lenders don’t just check your job—they analyze your career stability.

Risk Factors:

- Frequent job changes

- Short employment duration

- Working in unstable industries

Why It Matters:

Banks want assurance that you can repay the loan over time.

Hidden Insight:

Even high salary doesn’t help if your job is unstable.

Solution:

- Maintain at least 6 months stability

- Avoid applying immediately after switching jobs

- Provide complete employment proof

5. Industry Risk Profiling (Advanced 2026 Factor)

This is a new-age factor many people are unaware of. Banks now categorize industries based on risk.

High-Risk Categories:

- Small traders

- Freelancers without proof

- Startup employees

- Seasonal businesses

- Low-Risk Categories:

- Government employees

- MNC professionals

- Established businesses

👉 Your industry directly affects your approval chances.

Solution:

- Strengthen your income proof

- Show consistent earnings

- Provide additional documents if needed

Read More

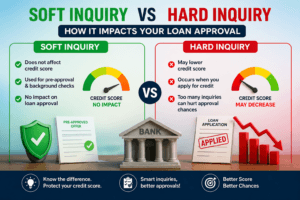

6. Hidden Impact of Multiple Loan Applications

Applying to multiple lenders seems logical—but it can hurt your profile.

What Happens:

- Each application triggers a hard inquiry

- Multiple inquiries reduce your creditworthiness

Bank’s Perspective:

“This applicant is credit hungry or financially stressed.”

Solution:

- Apply only after eligibility check

- Avoid applying to multiple lenders at once

- Wait between applications

7. Documentation Quality Matters More Than You Think

Even small documentation errors can lead to rejection.

Common Hidden Issues:

- Signature mismatch

- Address mismatch

- Incorrect income details

- Missing documents

Why It Matters:

Banks use automated systems that flag inconsistencies instantly.

Solution:

- Double-check all documents

- Ensure consistency across all records

- Keep updated KYC

8. Previous Loan Settlements or Write-Offs

This is one of the biggest hidden red flags.

What People Think:

“Settlement ho gaya, ab problem khatam.”

Reality:

Settlement indicates that you couldn’t repay fully.

Impact:

- Reduces trust

- Lowers approval chances

Solution:

- Always try to close loans fully

- Avoid settlements unless absolutely necessary

9. Digital Footprint & AI Risk Assessment

In 2026, loan approval is influenced by digital behavior.

What Lenders Analyze:

- Spending patterns

- Transaction consistency

- Financial discipline

Hidden Insight:

AI systems detect patterns that humans might miss.

Solution:

- Maintain clean transaction history

- Avoid suspicious or irregular transactions

10. Lack of Relationship with the Lender

Banks prefer customers they already know.

Hidden Disadvantage:

- New applicants = higher risk

- No transaction history = less trust

Solution:

- Maintain a bank account

- Build transaction history

- Use banking services regularly

11. Wrong Loan Product Selection

Many rejections happen because applicants choose the wrong loan type.

Example:

- Applying for high loan amount without eligibility

- Choosing a lender that doesn’t match your profile

Solution:

- Understand your eligibility

- Choose the right lender

- Take expert advice if needed

12. Psychological & Behavioral Risk Signals

This is the most hidden factor.

Banks indirectly assess:

- Financial discipline

- Risk-taking behavior

- Stability mindset

Indicators:

- Frequent borrowing

- Irregular payments

- Financial mismanagement

👉 These signals define your risk profile.

Frequently Asked Questions (FAQs)

1. What are the hidden reasons for loan rejection?

Hidden reasons include high credit utilization, unstable income, poor banking habits, and multiple loan applications.

2. Can a good CIBIL score still lead to rejection?

Yes, factors like FOIR, job stability, and financial behavior also play a major role.

3. How can I avoid loan rejection?

Maintain a strong credit profile, stable income, and apply only after checking eligibility.

4. How long should I wait after loan rejection?

You should wait at least 30–60 days after improving your profile before reapplying.

5. Does bank statement affect loan approval?

Yes, it is one of the most important factors used to assess your financial discipline.

Conclusion: Loan Approval is a Strategy, Not Luck

Loan rejection is not random—it is a calculated decision based on multiple visible and hidden factors.

In 2026, financial institutions are smarter than ever. They don’t just evaluate your income—they evaluate your financial personality.

👉 If you want approval:

- Think like a lender

- Maintain discipline

- Build a strong financial profile

Remember:

The stronger your financial behavior, the higher your approval chances.