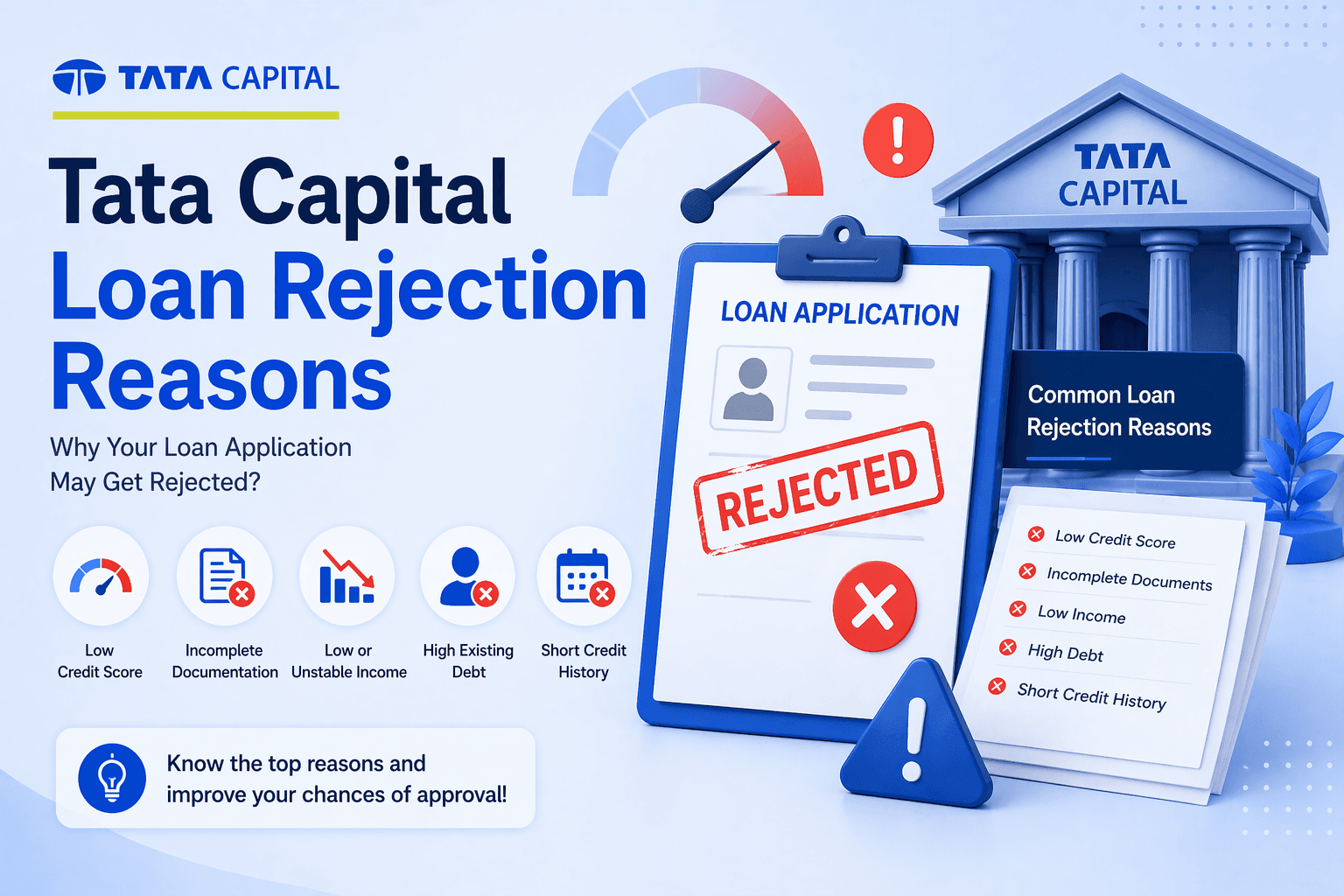

Tata Capital Loan Rejection Reasons

Applying for a personal loan from Tata Capital can seem straightforward — competitive interest rates, flexible tenures, and fast disbursal make it one of the popular choices in India. However, many applicants are left disappointed when their applications are denied. In fact, a large number of Tata Capital personal loan applications are rejected or declined, with many borrowers asking “Why did my loan get rejected?” or “What did I do wrong?”.

Table of Contents

ToggleIn this detailed guide, we’ll dive into the most common reasons why loans are rejected at Tata Capital, how the rejection affects your credit profile, what you can do to fix the problems, and how to improve your chances of approval next time.

Let’s get started!

Loan Rejection Is More Common Than You Think

Though “90%” rejection sounds dramatic, a significant number of first‑time applicants or applicants with weak financial profiles do get rejected because they fail to meet the lender’s criteria. A loan rejection isn’t the end — it’s an opportunity to understand the gaps in your financial profile and fix them.

Tata Capital, like most banks and non‑banking financial companies (NBFCs), uses a strict set of eligibility rules to assess a borrower’s financial health before approving a loan — and if these criteria aren’t met, the application gets declined.

1. Low Credit Score (CIBIL Score)

Most Common Reason:

A poor credit score is one of the biggest reasons your loan gets rejected. Lenders use your credit score to gauge your credit behaviour — whether you repay on time or delay payments.

If your CIBIL score is below 700, lenders see you as a high‑risk borrower.

A score below 650–680 often leads to automatic rejection.

Why does this happen?

Your credit score reflects your past repayment history, default records, and credit usage. A weak score signals that you might miss EMIs in the future, so Tata Capital may reject your loan request.

👉 Solution:

Check your credit report first and correct any errors. Pay pending EMIs/credit card bills and reduce credit utilization below 30%.

2. Insufficient or Inconsistent Income

Income Stability Matters:

Tata Capital evaluates whether your monthly income is sufficient to support the loan EMIs along with your other expenses.

If your income is below the minimum requirement or fluctuates significantly month to month, lenders may doubt your ability to repay the loan on schedule.

This is especially true for:

- Freelancers / gig workers

- Self‑employed professionals without steady earnings

- People with irregular or part‑time income

👉 Solution:

- Provide proof of stable earnings (bank statements, ITR)

- Show additional income sources if available

Read More: My Mudra Personal Loan-Apply online

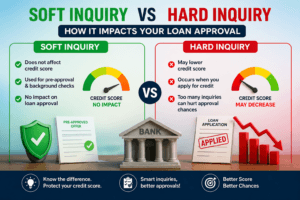

3. Too Many Loan or Credit Applications

Submitting multiple loan applications in a short time can hurt your chances. Every credit application creates a hard inquiry on your credit report, and multiple inquiries signal financial distress.

Example:

If you apply with multiple banks or NBFCs in a short span, Tata Capital might see this as a sign that you’re struggling financially — even if your income and credit score are good.

👉 Solution:

Apply selectively after checking your eligibility; give at least 3–4 months between applications.

4. High Existing Debt

Tata Capital examines your Debt‑to‑Income Ratio (DTI) or Fixed Obligations to Income Ratio (FOIR) — this measures how much of your income goes toward existing EMIs.

If your EMIs already consume most of your monthly income, the new loan could overburden you financially. Lenders often reject loans in such cases.

👉 Solution:

Reduce existing debts where possible, or wait until your EMIs drop to a manageable level before applying.

5. Incomplete or Incorrect Documentation

Missing, expired, or inconsistent documents are a quick way to get rejected. Tata Capital requires complete KYC and financial documentation such as:

- Aadhaar Card / PAN

- Salary slips / ITR / business proof

- Bank statement

- Proof of residence

If any document is missing or inaccurate, the application can be declined — even if other criteria are met.

👉 Solution:

Double‑check all uploaded documents before submission; ensure they are valid, clear, and match your application details exactly.

6. Employment Instability or Job Hopping

Frequent job changes, gaps in employment, or being self‑employed without a long business history can signal risk to lenders. They prefer profiles with stable employment history, which indicates predictable income and higher repayment capacity.

👉 Solution:

If possible, apply after completing at least six months with your current employer and maintain consistent bank credits.

7. Limited or Poor Credit History

If you have no or very limited credit history, lenders don’t have enough information to evaluate your repayment behaviour. This is common with younger borrowers or those who have never taken a credit card or loan before.

👉 Solution:

Build credit history gradually — start with a secured credit card or small loan that you repay on time.

Read More: Hidden Reasons for Loan Rejection

8. Internal Lending Policy & Risk Criteria

Every lender, including Tata Capital, has its internal credit policy — hidden rules that are not always publicly shared. These policies can include:

- Preferred minimum salary range

- Employment sectors they prefer or avoid

- Certain age limits

- Location restrictions

A rejection under “internal policy” does not always mean something is wrong with your profile — it may simply not match the bank’s risk appetite at that time.

👉 Tip:

Always ask Tata Capital for the exact reason listed in their rejection letter — lenders in India are required to disclose this within 30 days.

9. Mismatched Application Details

Even small discrepancies — wrong income entries, mismatched addresses, or name differences on documents — can lead to rejection. Banks are strict about accuracy in loan forms.

👉 Solution:

Review every detail carefully before submitting — ensure all personal info matches official documents.

10. Poor Financial Behaviour Seen in Bank Statements

Sometimes it’s not just your credit score — lenders also check bank account behaviour:

- Low balance patterns

- Frequent bounced cheques

- Irregular deposits

- Heavy cash withdrawals

These can signal financial instability even if your income and credit score look fine.

👉 Solution:

Maintain healthy banking habits for at least 6–12 months before applying.

What Happens After a Rejection?

A personal loan rejection from Tata Capital can feel discouraging, but it doesn’t lower your credit score itself. What does affect your score are multiple hard inquiries caused by reapplying too quickly.

Best Steps After Rejection:

- Ask Tata Capital for an official rejection reason.

- Check your credit report and fix issues.

- Reduce existing debts if possible.

- Improve banking behaviour and income documents.

- Wait at least 3–6 months before reapplying.

Tips to Improve Loan Approval Chances

Here’s how you can boost your chances of getting approved next time:

- Raise Your Credit Score

Pay EMIs and credit cards on time and keep utilization low.

2. Stabilize Your Income

A consistent employment record or steady business income reassures lenders.

3. Submit Complete Docs

Verify KYC, income proof, and bank statements before submission.

4. Avoid Too Many Applications

Focus on one well‑prepared application at a time.

5. Reduce Existing Debt

Lower your DTI ratio for better assessment.

FAQs (Frequently Asked Questions)

Q1. Can I reapply after being rejected by Tata Capital?

Yes, you can reapply after addressing the issues that caused the rejection. It’s best to wait at least 3–6 months before reapplying so your profile improves.

Q2. Does rejection hurt my CIBIL score?

No — a rejection itself doesn’t hurt your credit score, but multiple hard inquiries from frequent applications can.

Q3. What is the minimum CIBIL score Tata Capital requires?

While there is no official minimum, having a score above 700 greatly improves approval chances. Lower scores often lead to rejection.

Q4. Will incomplete documents cause rejection?

Yes. Missing or unclear documents are one of the top reasons lenders reject loans.

Q5. What’s a good income proof for personal loan?

Salary slips (last 3–6 months), bank statements, and income tax returns are commonly accepted proofs.

Conclusion

Getting a personal loan rejected by Tata Capital can be disheartening, but it’s usually a result of measurable eligibility issues — low credit score, insufficient income, incomplete documents, high debt levels, or internal risk policy criteria — not personal failure.

Understanding these reasons helps you do the right corrections, improve your financial profile, and come back stronger for approval next time. Focus on building your credit score, providing accurate documents, and applying only when you meet lender requirements — and you’ll see better results.

Loan rejection isn’t a dead end — it’s a chance to strengthen your financial habits and prepare a stronger application. with the right steps, you can significantly improve your chances of getting approved by Tata Capital or any other lender.